- Computer Concepts Tutorial

- Computer Concepts - Home

- Introduction to Computer

- Introduction to GUI based OS

- Elements of Word Processing

- Spread Sheet

- Introduction to Internet, WWW, Browsers

- Communication & Collaboration

- Application of Presentations

- Application of Digital Financial Services

- Computer Concepts Resources

- Computer Concepts - Quick Guide

- Computer Concepts - Useful Resources

- Computer Concepts - Discussion

Computer Concepts - Quick Guide

Computer Concepts - Introduction to Computer

In today's world, we use computers for all our tasks. Our day-to-day activities: paying bills, buying groceries, using social media, seeking entertainment, working from home, communicating with a friend, etc., can all be done using a computer. So it is important not only to know how to use a computer, but also to understand the components of a computer and what they do.

This topic explains all concepts related to computer in detail, from origin to end. The idea of computer literacy is also discussed, which includes the definition and functions of a computer. You learn about the components of a computer, the concept of hardware and software, representation of data/information, the concept of data processing and applications of IECT.

What is a Computer?

A computer is an electronic device that accepts data from the user, processes it, produces results, displays them to the users, and stores the results for future usage.

Data is a collection of unorganized facts & figures and does not provide any further information regarding patterns, context, etc. Hence data means "unstructured facts and figures".

Information is a structured data i.e. organized meaningful and processed data. To process the data and convert into information, a computer is used.

Functions of Computers

A computer performs the following functions −

Receiving Input

Data is fed into computer through various input devices like keyboard, mouse, digital pens, etc. Input can also be fed through devices like CD-ROM, pen drive, scanner, etc.

Processing the information

Operations on the input data are carried out based on the instructions provided in the programs.

Storing the information

After processing, the information gets stored in the primary or secondary storage area.

Producing output

The processed information and other details are communicated to the outside world through output devices like monitor, printer, etc.

| Sr.No. | Computer Concepts & Description |

|---|---|

| 1 | History of Computers

The history of the computer dates back to several years. There are five prominent generations of computers. Each generation has witnessed several technological advances which change the functionality of the computers. |

| 2 | Characteristics of Computer System

Characteristics of Computer System involve Speed, Accuracy, Diligence, Versatility, Reliability, Automation, Memory. |

| 3 | Basic Applications of Computer

Computers play a role in every field of life. They are used in homes, business, educational institutions, research organizations, medical field, government offices, entertainment, etc. |

| 4 | Components of Computer System

Computer systems consist of three components as shown in below image: Central Processing Unit, Input devices and Output devices. |

| 5 | Input Devices – Keyboard and Mouse

Input devices help to get input or data from user. |

| 6 | Other Input Devices

There are few other input devices which help to feed data to the computer. |

| 7 | Output Devices

Output devices help to display output to user |

| 8 | Computer Memory

Computer memory refers to storage area where data is stored. It is of two types Primary Memory & Secondary Memory. |

| 9 | Concept of Hardware and Software

The term hardware refers to mechanical device that makes up computer. Software can be categorized into two types - System software & Application software |

| 10 | Programming Languages

The languages that are used to write a program or set of instructions are called "Programming languages". Programming languages are broadly categorized into three types - Machine level language, Assembly level language, High-level language. |

| 11 | Representation of Data/Information

Computer does not understand human language. Any data, viz., letters, symbols, pictures, audio, videos, etc., fed to computer should be converted to machine language first. Computers represent that data into different forms. |

| 12 | Data Processing & Data Processing Stages

Data processing is a process of converting raw facts or data into a meaningful information. |

| 13 | Applications of IECT

IECT stands for Information Electronics and Communication Technology. |

Summary

In this chapter, we discussed different components of a computer, and familiarized ourselves with concept of hardware and software, representation of data/information, concept of data processing, and applications of IECT.

Introduction to GUI based Operating System

Personal computer has advanced a lot in a short period of time, and much of the advancement is due to ongoing progresses in operating systems. Evolution of operating systems had made PCs easier to use and understand, flexible and reliable. This chapter is the study of primary operating systems currently used in personal computers and network servers, and their basic features.

This topic presents a broad survey of concepts and terminologies related to operating systems like: Basics of operating system, user interface, basic settings of operating system, file & directory management, and types of files.

Basics of Operating System

Operating System

Operating system is a software that controls system’s hardware and interacts with user and application software.

In short, an operating system is computer’s chief control program.

Functions of Operating System

The operating system performs the following functions −

It offers a user interface.

Loads program into computer’s memory.

Coordinates how program works with hardware and other software.

Manages how information is stored and retrieved from the disk.

Saves contents of file on to disk.

Reads contents of file from disk to memory.

Sends document to the printer and activates the printer.

Provides resources that copy or move data from one document to another, or from one program to another.

Allocates RAM among the running programs.

Recognizes keystrokes or mouse clicks and displayes characters or graphics on the screen.

| Sr.No. | Operating System Concepts & Description |

|---|---|

| 1 | Types of Operating System

There are four types of operating systems. |

| 2 | Basics of Popular Operating Systems

Windows Operating System is developed by Microsoft Corporation, Linux is a multitasking operating system that supports various users and numerous tasks. It is open source, i.e., code for Linux is available for free of cost |

| 3 | User Interface

While working with a computer, we use a set of items on screen called "user interface". In simple terms, it acts as an interface between user and software application or program |

| 4 | Running an Application

The operating system offers an interface between programs and user, as well as programs and other computer resources such as memory, printer and other programs. |

| 5 | Operating System Simple Setting

We will learn different settings in Operating System such as changing system date and time, changing display properties, etc. |

| 6 | File and Directory Management

File is nothing but a collection of information. The information can be of numbers, characters, graphs, images, etc. Directory is a place/area/location where a set of file(s) will be stored. |

| 7 | File Management System

The file management system is a software which is used to create, delete, modify and control access and save files. |

| 8 | Types of Files

There are five types of files such as Ordinary files, Directory files, Device files, FIFO files |

Summary

This topic had given a detailed description of operating system, user interface, changing simple settings in the operating system, files & directory management and types of files.

Elements of Word Processing

Microsoft Word is a popular word processing software. It helps in arranging written text in a proper format and giving it a systematic look. This formatted look facilitates easier reading. It provides spell-check options, formatting functions like cut-copy-paste, and spots grammatical errors on a real-time basis. It also helps in saving and storing documents.

It’s also used to add images, preview the complete text before printing it; organize the data into lists and then summarize, compare and present the data graphically. It allows the header and footer to display descriptive information, and to produce personalized letters through mail. This software is used to create, format and edit any document. It allows us to share the resources such as clip arts, drawing tools, etc. available to all office programs.

In this chapter, you will learn about Concepts related to MS Word in detail. You will know about Word Processing Basics, Opening and Closing the Document, Text Creation and Manipulation, Formatting Text, and Table Manipulation.

Basics of Word Processing

Word processor is used to manipulate text documents. It is an application program that creates web pages, letters, and reports.

| Sr.No. | Word Processing Concepts & Description |

|---|---|

| 1 | Opening Word Processing Package

Word processing package is mostly used in offices on microcomputers. To open a new document, click on "Start" button and go to "All Programs" and click on "Microsoft Word". |

| 2 | Opening and Closing Documents

Word automatically starts with a blank page. For opening a new file, click on "New". |

| 3 | Page Setup

Page setup options are usually available in "Page Layout" menu. Parameters defined by the user help in determining how a printed page will appear. |

| 4 | Print Preview

This option is used to view the page or make adjustments before any document gets printed. |

| 5 | Cut, Copy and Paste

In this section, we shall learn how to use cut, copy and paste functions in Word. |

| 6 | Table Manipulation

Manipulation of table includes drawing a table, changing cell width and height, alignment of text in the cell, deletion/insertion of rows and columns, and borders and shading. |

Summary

This topic provides us with a clear idea about components of word processing basics, opening and closing the documents, text creation and manipulation, formatting the text, table manipulation, etc.

Computer Concepts - Spread Sheet

Microsoft Excel is a spreadsheet application which is used to create and manage lists of information. Excel allows to enter, edit, manage and analyze large amount of data in a worksheet and create colorful charts and graphs. It uses formulae to calculate and analyze data. It helps to combine a series of commands using "Macros", thus saving time. At higher levels, you can use it as a complete development tool catering to many complex requirements.

| Sr.No. | Spread Sheet Concepts & Description |

|---|---|

| 1 | Elements of Electronic Spread Sheet

The topics explaining the entire concepts related to spread sheet in detail, i.e., Elements of an electronic spread sheet, manipulation of cells, functions and charts. |

| 2 | Manipulation of Cells

Manipulation of cells is entering and modifying the contents of the cells. |

| 3 | Creating Text, Number and Date Series

Here, we will look into how to create text series, how to create number series and how to create data series |

| 4 | Editing Worksheet Data

Modifying or adding text or using cut, copy, paste operations to an existing document is known as editing. |

| 5 | Function and Charts

We shall learn how to use functions and charts in Microsoft Excel Using Formulas like Addition, Subtraction, Multiplication, Division |

| 6 | Chart

A chart is a graphical representation of worksheet data. Charts can make data interesting, attractive and easy to read and evaluate. They can also help you to analyze and compare data. |

Example Program

We shall discuss an example to understand this concept −

Aim

To prepare a bar chart.

Procedure

Click Start → All programs → MS-Office → MS-Excel.

Insert a table in the worksheet.

Select Insert → Chart icon.

Select column option from chart type.

In the title bar, Click on chart title box and type, population of metropolitan cities.

Result

The given database is created in excel worksheet using the bar chart.

Summary

This topic had given detailed description about the concepts of opening new and existing worksheets, renaming the work sheet, organizing spread sheet, printing spread sheet, saving workbooks, manipulation of cells, entering text, numbers and dates, creating text, number and date series, editing worksheet data, inserting and deleting rows & columns, changing cell height and width, using formulas, and creating a chart. This chapter also focused on cell address, numbers and text, title bar, menu bar, formula bar, and functions & charts.

Introduction to Internet, WWW and Web Browsers

Internet is a global communication system that links together thousands of individual networks. It allows exchange of information between two or more computers on a network. Thus internet helps in transfer of messages through mail, chat, video & audio conference, etc. It has become mandatory for day-to-day activities: bills payment, online shopping and surfing, tutoring, working, communicating with peers, etc.

In this topic, we are going to discuss in detail about concepts like basics of computer networks, Local Area Network (LAN), Wide Area Network (WAN), concept of internet, basics of internet architecture, services on internet, World Wide Web and websites, communication on internet, internet services, preparing computer for internet access, ISPs and examples (Broadband/Dialup/Wi-Fi), internet access techniques, web browsing software, popular web browsing software, configuring web browser, search engines, popular search engines/search for content, accessing web browser, using favorites folder, downloading web pages and printing web pages.

| Sr.No. | Internet, WWW, Web Browsers Concepts & Description |

|---|---|

| 1 | Basics of Computer Networks

Computer network is an interconnection between two or more hosts/computers. Different types of networks include LAN, WAN, MAN, etc. |

| 2 | Internet Architecture

Internet is called the network of networks. It is a global communication system that links together thousands of individual networks. Internet architecture is a meta-network, which refers to a congregation of thousands of distinct networks interacting with a common protocol |

| 3 | Services on Internet

Internet acts as a carrier for numerous diverse services, each with its own distinctive features and purposes. |

| 4 | Communication on Internet

communication can happens through the the Internet by using Email, Internet Relay Chat, Video Conference etc. |

| 5 | Preparing Computer for Internet Access

We shall learn how to use functions and charts in Microsoft Excel Using Formulas like Addition, Subtraction, Multiplication, Division |

| 6 | Internet Access Techniques

A chart is a graphical representation of worksheet data. Charts can make data interesting, attractive and easy to read and evaluate. They can also help you to analyze and compare data. |

| 7 | Web Browsing Software

"World Wide Web" or simple "Web" is the name given to all the resources of internet. The special software or application program with which you can access web is called "Web Browser". |

| 8 | Configuring Web Browser

Search Engine is an application that allows you to search for content on the web. It displays multiple web pages based on the content or a word you have typed. |

| 9 | Search Engines

Search Engine is an application that allows you to search for content on the web. It displays multiple web pages based on the content or a word you have typed. |

| 10 | Search for the content

Search Engine helps to search for content on web using the different stages |

| 11 | Accessing Web Browser

There are several ways to access a web page like using URLs, hyperlinks, using navigating tools, search engine, etc. |

Summary

This topic summarized the concepts of internet like LAN, WAN, internet architecture, internet services, WWW, communications on the internet, internet service providers, internet access techniques, web browsers, search engines, favourites folder, configuration of web browsers, and downloading & printing web pages.

Communication and Collaboration

Communication refers to exchange of information between persons through internet. Internet provides a basis for communication and collaboration which can be done using mail, chat, skype, etc. When dealing with official matters, electronic mail helps in the exchange of messages text documents, web pages, audio, video, etc.

In this topic, we are going to discuss in detail about basics of email, email addressing, configuring email client, using emails, opening email client, mailbox, creating and sending a new email, replying to an email message, forwarding an email message, sorting and searching emails, advance email features, sending documents by email, activating spell check, using address book, sending softcopy as attachment, handling spam, instant messaging and collaboration, using emoticons and some of the internet etiquettes.

Basics of E-mail

Electronic mail is an application that supports interchange of information between two or more persons. Usually text messages are transmitted through email. Audio and video transfer through email depends on the browser in use. This provides a faster way of communication in an affordable cost.

Advantages of E-mail

Functionalities like attachment of documents, data files, program files, etc., can be enabled. This is a faster way of communication at an affordable cost.

Disadvantages of E-mail

If the connection to the ISP is lost, then you can’t access email. Once you send an mail to a recipient, you have to wait until she/he reads and replies to your mail.

Email Addressing

Email address is a unique address given to the user that helps to identify the user while sending and receiving messages or mails.

Username − Name that identifies any user’s mailbox

Domain name − Represents the Internet Service Provider (ISP).

@ Symbol − Helps to concatenate username and domain name.

For example − user_name@domain_name

Username − user, Domain name − gmail.com

| Sr.No. | Communication and Collaboration Concepts & Description |

|---|---|

| 1 | Configuring Email Client

Configuring email client is setting up a client which includes the various steps. |

| 2 | Using E-mails

The main purpose of using email is to exchange information between persons. The process starts with opening of client email and ends with sending and verifying mail to recipients. |

| 3 | Mailbox: Inbox and Outbox

Inbox is an area where you can see all the received mails. Outbox is an area where the outgoing messages or messages which are in process of sending or which are failed to send are stored. |

| 4 | Advance Email Features

Email provides many advanced features which includes sending attachments like documents, videos, images, audio, etc. |

| 5 | Instant Messaging and Collaboration

Instant messaging is real time mutual communication between persons via internet. This is a private chat. Once the recipient is online, you can start sending messages to him/her. |

| 6 | Internet etiquettes

Internet etiquettes are also called as "Netiquette".Netiquettes are basic rules or techniques which are accepted worldwide |

Summary

This chapter has given a clear idea about the electronic mail and its features. Thus, we gained a deep understanding about the basics of email, email addressing, configuring email client, using emails, opening email client, mailbox, creating and sending a new email, replying to an email message, forwarding an email message, sorting and searching emails, advance email features like sending document by email, activating spell check, using address book, sending softcopy as an attachment, handling SPAM, Instant Messaging and Collaboration, using smiley/emoticons and some internet etiquettes.

Computer Concepts - Application of Presentations

Microsoft PowerPoint is one of the powerful tools of MS-Office, which helps in creating and designing presentations. PowerPoint Presentation is an array of slides that convey information to people in an attractive manner.

In this chapter, we are going to discuss in detail about the applications of presentation using Microsoft PowerPoint, opening and saving a presentation, creating presentation using templates and a blank presentation, entering and editing text, inserting and deleting slides in a presentation, preparing slides, inserting word table or an excel worksheet and other objects, adding clip arts, resizing and scaling of objects, providing aesthetics by enhancing text presentation, working with colors and line style, adding movie and sound, header and footer, viewing a presentation, choosing a set up for presentation, printing slides and handouts, Slide Show, running a Slide Show, transition and slide timings, automating a Slide Show.

| Sr.No. | Application of Presentations Concepts & Description |

|---|---|

| 1 | Using Powerpoint

Microsoft PowerPoint is one of the powerful tools of MS-Office, which helps in creating and designing presentations |

| 2 | Creation of Presentation

A presentation is made up of number of slides that are displayed in a sequence. Each slide has sub-topics and different content related to the given topic. |

| 3 | Preparation of slides

Preparation of slides involves inserting a word table, excel worksheet, adding clip art pictures and inserting other objects |

| 4 | Providing Aesthetics

This feature helps our Powerpoint presentation to look more attractive and interesting. |

| 5 | Program Example

Here will create a simple presentation with at least 5 slides to introduce a friend and include audio in slides. |

| 6 | Presentation of Slides

Presentation of Slides has the feature like Viewing a presentation, choosing a set up for presentation, Printing slides etc |

| 7 | Slide Show

Slide Show view of the presentation is used to display content of presentation to the audience. Editing is not possible in the Slide Show view. |

Example Program

We will look at the below example to understand the concept clearly −

Aim

To create a simple presentation with at least 5 slides on the essay, "An astrologer's day" by R. K. Narayan.

Procedure

Boot the system under Microsoft Windows 2013.

Click start → program → MS-Office → MS-PowerPoint.

Once you open PowerPoint, choose the type of presentation you want and click Ok.

Select Insert → Text box.

Draw the text box in the slide and enter information about the essay, "An astrologer's day".

Right click on the text box and select custom animation in it.

Select an effect and click ok.

Right click in the empty space of the slide.

Select background color and click apply button.

Click Transition select an effect and press ok.

Click the first slide and drag the mouse to select all the slides.

Run your presentation by clicking on "From Beginning" option from Slide Show or by pressing F5 key.

Result

Thus, a simple presentation for the essay "An astrologer's day" by R.K.Narayan is created.

Summary

In this chapter, we have clearly learnt various concepts in PowerPoint presentation such as opening and saving a presentation, creating presentation using templates and a blank presentation, entering and editing text, inserting and deleting slides in a presentation, preparing slides, etc.

Application of Digital Financial Services

In today's world, everything is digitized, which means we can access or get every service in digital format through mobile phones, computers, tablets, etc. The invention of computers and smartphones has created a huge impact on financial services. Today using computers and mobile phones, a person can access his/her bank account, verify account details, transfer funds, deposit cash, renew deposit, pay bills, book tickets, etc. Also, the invention of ATMs reduced the time taken to withdraw money from banks. Digital services help to save time by providing services in a single touch. The introduction of digital wallets has also made a big positive impact on financial services.

In this topic, we are going to discuss in detail the importance of savings, importance of bank, banking products like accounts, deposits, loans, procedure for opening an account, banking services through a bank branch, ATM, internet banking, mobile banking, mobile wallets, insurance and various schemes introduced by the Prime Minister of India.

Why are savings needed?

Savings is the percentage of income which is not spent on present expenditures, instead conserved for future use. Being totally unaware of the future happenings, one should be ready to face any kind of unpredictable events. In such tough situations, our savings will be very helpful and beneficial to us.

Emergencies

Emergencies may come at anytime and we should always have a backup to handle such situations. Some examples of emergencies from our day to day life are −

Personal and family health issues.

Loss due to sudden natural calamities like flood, earthquake or cyclone, etc.

Loss due to theft or any other unanticipated events.

Sudden financial help for friends or relatives.

Unplanned trips or any other plans.

Future Needs

Few future needs are listed below −

Retirement

The main purpose to save money is for your retirement. The earlier you start saving for retirement, the less you have to save in future. Saving for retirement makes you self-dependent and financially secure.

Own a property

Everyone dreams of owning a house. Though it is not an easy task, saving from early stages can help in fulfilling this dream.

Own your own vehicle

In today's scenario, transportation has become difficult in metropolitan cities. To explore places with ease and comfort, a person needs a car.

Education

Cost of education has become a burden these days, especially for higher studies. In order to attain higher degrees, one should save money.

To rescue debts and large expenses

We should start saving to deal with large expenses like −

Buying property: house or land

Buying vehicles

Buying gold or expensive jewelry

Handling emergency needs like health-related issues

Going on a family tour

Facing complex situations during natural calamities

Drawbacks of keeping cash at home

Here, we list certain drawbacks of maintaining cash at home −

Unsafe

It is unsafe to keep cash at home as there is a chance of theft or robbery.

Loss of Growth Opportunity

Keeping cash at home causes huge loss to the country's economy as it does not participate in national growth.

Recurring Deposit −It is referred to as a monthly deposit for particular period of time for which the interest will be provided by banks to their customers.

Fixed Deposit −It is bulk amount deposited by the customer for a fixed period of time, i.e., an year or two.

In any of the schemes provided by banks, there will be profit.

We can even earn interest or dividend by depositing our money in saving bank account.

No Credit Eligibility

A person should have minimum balance in savings account to apply for credit cards or loans.

If we save money at home instead of banks, we can't avail the credit facility provided by the financial institutions during tough times.

Why is bank needed?

Bank is an official financial institution that accepts money from public and lends money to public.

Secure Money, Earn Interest, Get Loan

Bank functions in various ways. Few of them are listed below −

Secure Money

Bank helps to save our money very securely.

Loading all your cash at home isn't safe.

You can loose your money in situations like fire, flood or earthquake

In order to avoid the scenarios given above, we need a bank.

Earn interest

Banks provide us with interest if we save money through RD and FD. In any of the schemes provided by the bank there will be an opportunity of growth in our money.

Get Loan

Bank will provide several kinds of loans if we satisfy the criteria issued by a bank and submit all necessary documents. Types of loans provided by bank are −

Home Loan − Home loan is the money lent by banks to buy properties at a certain rate of interest to be paid every month as EMI.

Personal Loan − Banks provide you with personal loans for marriage, emergency periods, etc.

Jewel Loan − Banks provide you with jewel loans where you pledge your jewelry to get loan.

Remittances using Cheque and Demand Draft

Remittance is defined as the transfer of money or funds from one bank to another, either the same bank or different. Remittance can be done using Demand draft by Cheque, Pay slip, Mail Transfer, etc. A demand draft or "DD" is a popular mode of money transfer, where most of the banks in India use this for the effective transfer of money. Demand draft is usually issued on request of the client, for bill payments, and for transfer of property of deceased to legal heirs, etc. DD form requires the following details to be filled by the customer −

Type of instrument needed.

Receiver's Name.

Transmitter's Name.

Total amount to be transferred.

The bank or location where the transferred money is to be funded.

The way money is to be paid, i.e. in "Cash" or through a "Bank Account" in which you will pay money, i.e. in cash or by debit to your account.

You should submit form along with cheque or cash.

Avoid risk of Chit Funds and Sahukars

Using banks to save money, we can avoid the below stated risks −

Chit Fund

Chit funds are local bodies which help to save money. It is run by one or more people of that area. Chit fund is purely based on trust. It is easy to join the chit fund because no proper background is needed except some paperwork. If you deposit money in chit fund you can take out that money whenever you need. Instead, in banks you must wait until the time period get completed.

Risk in saving money in chit funds or Sahukars

Chit funds are not authorized parties to deposit money.

People who are running chit funds can wind up their chit fund if they wish to do so.

There are chances of loss or theft of money.

There is no security or assurance for the money you deposit in chit funds.

There is a chance that the fund manager disappears with mass amount.

A member could disappear after winning the first bid.

Banking Products

We shall learn various banking products −

Accounts

An agreement with a bank, where an account holder can deposit and withdraw money or savings as needed.

Types of Accounts

There are three types of accounts avaliable, namely −

Personal account

Account that represents an individual or an organization is termed as "Personal account". Examples: Mr. Rama's account → Individual persons account; Samsung's account → Organization's account.

Real account

The account that represent tangible assets, that is, which can be physically sensed, is termed as "Real account". Examples include: cash, goods, stock accounts, etc.

Nominal account

Account that represents expenses and incomes is termed as "Nominal account". Examples include: salary, loss of asset accounts, etc.

Deposit

Accumulation of money in the bank is termed as deposits. There are two types of deposits: Time deposit and Demand deposit. Time deposit is defined as money deposited for a particular period of time which cannot be withdrawn before the time gets lapsed.

Fixed deposit − A bulk amount is deposited for a fixed period like a year or two years etc.

Re-investment deposit − Interest is accumulated quarterly and paid on maturity.

Recurring deposit −Fixed amount is deposited at regular intervals like a month or quarterly etc.

Demand deposit is the scheme where the customer can withdraw money on demand without earlier notice to the bank. Demand deposit may or may not provide interest to the customer. Examples of demand deposits include current account and a savings account.

Types of Loan and Overdrafts

Loan is termed as the fund lent to a person on having a promise that he/she will return the money within a certain period with interest. Loan falls under the following categories.

Secure Loan is a loan where the borrower pledges any of his/her assets like house, land, jewel or any of the belongings as security. The financial institution has a right to sell these if repayment is not done on time.

Unsecure Loan is where the borrower does not submit any of the belongings as security to the bank. The example includes peer-peer lending, personal loans, credit debts, etc.

Demand Loan is a loan where a person borrows money on demand. It doesn't fix return time.

Educational Loan is money borrowed to support one's education. He/she doesn't have to repay the money while studying.

Personal Loan is a loan that is borrowed based on personal interest for marriage, world tour, other expenses, etc.

Commercial Loan is lent to an organization for improvement purposes.

Overdraft

An overdraft is a condition that occurs when a person attempts to withdraw money from zero balance account. The types of overdraft include −

Secured Overdraft −Secure overdraft is where the customer pledges any of his/her assets to bank as security.

Unsecure Overdraft − Unsecure overdraft is the one where the customer does not submit any of the belongings as security to the bank.

Filling up of Cheque, Demand Drafts

We will separately learn how to fill cheques and demand drafts below −

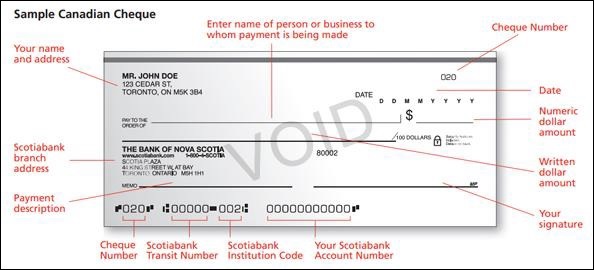

Filling up of Cheque

You must provide the following details while filling a cheque.

Write date at the top right corner of your cheque.

Write name of the receiver to whom the cheque is to be encashed.

Write the amount both in numbers as well as words.

Put your signature at bottom left corner of the cheque.

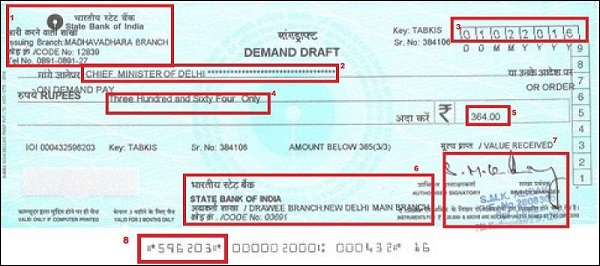

Filling up of Demand Drafts

You must provide the following details while filling a demand draft.

Type of instrument needed.

Receiver's Name.

Transmitter's Name.

Total amount to be transferred.

The bank or location where the transferred money is to be funded.

Mode of transaction, i.e. in "Cash" or through a "Bank Account" in which you will pay money, i.e. in cash or by debit to your account.

You should submit the form along with cheque or cash.

Documents for Opening Accounts

You need the below documents to open account in banks −

Know your Customer (KYC)

Know your Customer is a process in which banks acquire details about the identity and address of the customers. It is practice accomplished by banks when you open an account with that bank. Banks in regular intervals will update their customer details. The KYC process helps to make sure that the bank services are not misused.

Photo ID Proof, Address Proof

RBI issues a certain norm to be followed while opening an account. One of that is KYC during account opening. We should be providing ID proof and Address proof during the KYC process.

ID Proof − KYC process accepts Voter ID card, Aadhaar Card, Driving license, PAN card, Passport, etc., as ID proof.

Address Proof − Ration card, rental agreement, gas book, telephone bill, voter ID, Aadhar card, etc., are accepted as address proof.

Indian Currency

Indian currency is issued by "Reserve Bank of India". Indian rupee is the official currency of India. The word "Rupee" is the derivative of the Sanskrit word "Rupya" (meaning silver coin). It is denoted by the code "INR". We have 10, 20, 50, 100, 200, 500, 2000-rupee notes and 1, 2, 5, 10-rupee coins.

Banking Service Delivery Channels - I

We shall learn different banking service delivery channels in this section −

Bank Branch and ATM

Bank branch is one of the easiest and simplest ways of providing banking services. Every area has one or more bank branches depending on the space coverage of the area through which we can access bank services. We can go to the branch physically and avail services like money deposit or withdrawal, salary update, pension withdrawal, etc.

Automatic Teller Machine has reduced lot of human workload. This is one of the cheapest sources of bank delivering 24/7 service. This facilitates us with the service of money withdrawal. We also have cash deposit machines, passbook update machines, etc.

Bank Mitra with Micro ATM

Bank Mitra is also called as "Customer Service Point". Mitra provides services like account opening, cash deposit, cash withdrawal, fund transfer, etc., and is a representative of mini bank which provides services to rural areas. It especially provides services to villages where no bank branches are available.

Point of Sales

Point of Sales (POS) support for real-time transactions. Suppose if you are purchasing anything in shops and decided to use your debit card, the consumer will be having a POS machine in which your debit/credit card is swiped to deduct the amount for your purchase. This provides cashless transaction facility.

Banking Service Delivery Channels - II

This section deals with online delivery channels −

Internet Banking

Internet banking helps to save your time by providing digital services like −

Transfer funds from your account to another account.

Verify your bank account particulars and statements.

Make payment of utility and credit card bills.

Open and renewal of fixed deposit account.

Recharge and payments of daily needs like prepaid mobile/DTH, train bookings or bus tickets, etc.

National Electronic Fund Transfer (NEFT)

National Electronic Fund Transfer is a nationwide fund transfer system formulated and maintained by RBI. It helps to transfer funds between customers of the bank across the country. It was started in the year 2005. NEFT follows batch wise fund transfer process that it works from 8.00 AM to 6.30 PM on Monday to Saturday excluding 2nd, 4th Saturday and government holidays.

Real Time Gross Settlement (RTGS)

Real Time Gross Settlement (RTGS) is a real-time electronic fund transfer system between banks. Unlike NEFT which follows a batch process, RTGS helps to transfer funds in real-time and gross basis. Real-time settlement refers to that there is no waiting time for the money to get transferred. Gross refers to one-to-one transaction. The minimum amount to be transferred through RTGS is 2,00,000 rupees. Apart from money this helps to transfer securities (tradable financial asset).

Immediate Payment Services (IMPS)

Immediate Payment Services (IMPS) was launched in the year 2010. IMPS is available 24/7 and even on holidays. IMPS is managed by National Payments Corporation of India. It offers interbank electronic fund transfers and it is accepted by almost all banks and financial institutions.

Insurance

Insurance is an agreement to deliver a compensation amount by the financial institution for certain loss, destruction, ailment, or demise in return for payment of a specified premium.

Necessity of Insurance

Insurance is protection for financial loss and provides medical support in case of severe ailments. It provides safety and security to human life as well as business. It generates financial resources, encourages savings by investing regular premium and promotes economic growth by mobilizing domestic savings. Insurance. Insurance accelerates economic growth by collecting and investing funds in industrial development. Insurance helps to get loans. Insurance helps in medical emergencies.

Life Insurance and Non-Life Insurance

In the subsequent section, we shall discuss various about various Life Insurance schemes and various other schemes −

Life Insurance

An agreement to deliver compensation amount by the financial institution on demise of an insured person in return for payment of a specified premium.

Necessity for Life Insurance

To give heirs a financial support after a person's demise.

To protect your family and loved ones.

To pay off debts taken by you.

To support uncertainties in life.

Non-life Insurance

General or non-life insurance saves individual against uncertainties, loss, destruction and damage caused by natural events.

Necessity for Non-Life Insurance

It provides peace of mind to the insured person or business man.

It replaces lost income, destroyed property or damaged objects.

Pradhan Mantri Jan-Dhan Yojana (PMJDY)

Pradhan Mantri Jan-Dhan Yojana (PMJDY) is launched by Prime Minister of India, Narendra Modi on 28 August 2014.PMJDY is a National Mission for Financial Inclusion to ensure access to financial services, namely, Banking/Savings & Deposit Accounts, Remittance, Credit, Insurance and Pension in an affordable manner. Account can be opened in any bank branch or Business Correspondent outlet. PMJDY accounts are being opened with zero balance. However, if the account-holder wishes to get cheque book, he/she will have to fulfill minimum balance criteria.

Benefits of PMJDY

Interest on deposit

Accidental insurance cover of Rs. 1.00 lakh

No minimum balance required

Life insurance cover of Rs.30,000/-

Easy transfer of money across India

Beneficiaries of Government Schemes will get a direct benefit transfer in these accounts.

After satisfactory operation of the account for 6 months, an overdraft facility will be permitted.

Access to pension, insurance products

Accident insurance cover, repay debit card must be used at least once in 45 days.

Overdraft facility up to Rs.5000/- is available in only one account per household, preferably lady of the household.

Social Security Schemes

There are lots of social security schemes launched by the Prime Minister "Narendra Modi". Some of the important schemes are described in detail below.

Pradhan Mantri Suraksha Bima Yojana (PMSBY)

The scheme offers to provide you or your family a cover of up to Rs. 2 lakhs in case of any accidents, resulting in death or disability of the insured. In case of death or full disability, you or your family will get Rs. 2 lakhs and in case of partial disability, you will get Rs.1 lakh. Full disability means loss of both eyes, both legs, both hands, whereas partial disability means loss of one eye or leg or hand.

Age of the Insured – Savings bank account holders aged between 18 years and 70 years are eligible to apply for this scheme. People aged more than 70 years will not be able to get the benefits of this scheme.

Premium Amount – It costs you just Rs. 12 in annual premiums for having an accidental death or disability cover of Rs. 2 lakhs under this scheme. It works out to be just Re. 1/month, which is extraordinarily low. Again, your age has nothing to do with the premium payable for your insurance cover under this scheme as the premium is fixed at Rs. 12 for a cover of Rs. 2 lakhs.

Period of Insurance – You will remain insured for a period of one year from June 1, 2015 to May 31, 2016. Next year onwards, the risk cover period will remain to be June 1 to May 31.

Administrators for PMSBY– The scheme would be offered/administered by many general insurance companies, both in the public sector as well as in the private sector. Participating banks will be free to engage any such general insurance company for implementing the scheme for their subscribers. National Insurance Company Limited, Oriental Insurance Company Limited and ICICI Lombard are some of the companies which would be offering this scheme.

Auto Debit Facility – You will be required to provide your consent for auto debit of Rs. 12 as the annual premium from any one of your bank accounts at the time of enrolling for this scheme. This premium of Rs. 12 will get deducted from your savings bank account through auto debit facility every year between May 25 and June 1.

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) is a "Life insurance" coverage by "Government of India". The following are the features of this life insurance scheme −

Age of the Insured – Bank account holders aged between 18 and 50 years are eligible to apply in this scheme. So, if you are aged more than 50 years, you are not eligible to enroll yourself in this scheme. But, once enrolled, you can continue with this scheme till you attain the age of 55 years.

Premium Amount – Less than Re. 1 a day or an annual premium of Rs. 330 is what you need to pay to get a life cover of Rs. 2 lakhs. No matter what your age is, the premium is fixed at Rs. 330 for a life cover of Rs. 2 lakhs. This annual premium of Rs. 330 has been fixed for the first three years from June 1, 2015 to May 31, 2018, after which it will be reviewed again based on the insurers' annual claims experience.

Period of Insurance – June 1st, 2015 to May 31st, 2016 is the period for which this scheme will cover all kinds of risks to your life in the first year of operation. Next year also, the risk cover period will be from June 1 to May 31.

Auto Debit Facility – Annual premium of Rs. 330 will get deducted from your savings bank account through auto debit facility. You will have to give your consent for auto debit of premium from any one of your bank accounts at the time of enrolling for this scheme.

Atal Pension Yojana (APY)

The Government of India is concerned about the old age income security of the working poor and is focused on encouraging and enabling them to save for their retirement. To address the longevity risks among the workers in the unorganized sector and to encourage the workers in the unorganized sector to voluntarily save for their retirement, the Government of India has announced a new scheme called Atal Pension Yojana (APY) in 2015-16 budget. The APY focuses on all citizens in the unorganized sector. The scheme is administered by the Pension Fund Regulatory and Development Authority (PFRDA) through NPS architecture.

Eligibility for APY − Atal Pension Yojana (APY) is open to all bank account holders who are not members of any statutory social security scheme.

Age of joining and contribution period − The minimum age of joining APY is 18 years and the maximum age is 40 years. One needs to contribute till he/she attains 60 years of age.

Enrollment agencies − All Points of Presence (Service Providers) and Aggregators under Swavalamban Scheme would enroll subscribers through the setup of the National Pension System.

If a person joined Atal Pension Yojna at 35 years, he will contribute till the age of 60 years i.e. for 25 years. If he wants monthly pension of Rs. 1000 he would contribute Rs. 181 a month. On his death his wife will receive Rs. 1000 per month and after her death the nominees will get 1.7 lakh. If he wants monthly pension of Rs.3000 he would contribute Rs. 543 a month. On his death, his wife would get Rs. 3000 per month and after a death the nominees will get 5.1 lakh.

Pradhan Mantri Mudra Yojana (PMMY)

Prime Minister Narendra Modi launched Micro Units Development and Refinance Agency Ltd (MUDRA) Bank on 8 April, 2015 with a corpus of Rs. 20,000 crore and a credit guarantee corpus of Rs. 3,000 crore. The launch was the fulfilment of an announcement made earlier by the Finance Minister Mr. Arun Jaitley in his FY 15-16 Budget speech.

Objectives of PMMY

Regulate the lender and the borrower of microfinance and bring stability to the microfinance system through regulation and inclusive participation.

Extend finance and credit support to Microfinance Institutions (MFI) and agencies that lend money to small businesses, retailers, self-help groups and individuals.

Register all MFIs and introduce a system of performance rating and accreditation for the first time. This will help last-mile borrowers of finance to evaluate and approach the MFI that meets their requirements better and whose past record is most satisfactory. This will also introduce an element of competitiveness among the MFIs. The ultimate beneficiary will be the borrower.

Provide structured guidelines for the borrowers to follow to avoid failure of business or take corrective steps in time. MUDRA will help in laying down guidelines or acceptable procedures to be followed by the lenders to recover money in cases of default.

Develop standardized covenants that will form backbone of the last-mile business in future.

Offer a Credit Guarantee scheme to provide guarantee to the loans which are being offered to micro businesses.

Introduce appropriate technologies to assist in the process of efficient lending, borrowing and monitoring of distributed capital.

Build a suitable framework under the Pradhan Mantri MUDRA Yojana for developing an efficient last-mile credit delivery system to small and micro businesses.

National Pension Scheme

National Pension Scheme is a voluntary defined contribution pension system. NPS is administered and regulated by the Pension Fund Regulatory and Development Authority (PFRDA). NPS is the most economical pension scheme for Indian citizens between 18-60 age group. The more the invested money, the more the accumulated pension. A citizen of India, whether resident or non-resident can avail NPS facility. The NPS is applicable to central government employees, state government employees, corporate, individual, unorganized sector workers - Swavalamban Yojana. NPS helps to protect your future and get tax benefits.

Components of National Pension System

Point of Presence (POP) − The authorized branches of a POP, called Point of Presence Service Providers (POP-SPs) act as collection points and extend a number of customer services to NPS subscribers.

Central Recordkeeping Agency (CRA) − This provides recordkeeping, administration and customer service functions for all subscribers of the NPS.

Pension Funds (PFs)/Pension Fund Managers (PFMs) − The six Pension Funds (PFs) appointed by PFRDA would manage your retirement savings under the NPS.

Trustee Bank − The Trustee Bank appointed under NPS shall facilitate fund transfers across various entities of the NPS system.

Annuity Service Providers (ASPs) − ASPs would be responsible for delivering a regular monthly pension after you exit from the NPS.

NPS Trust − A Trust, appointed under the Indian Trusts Act, 1882 is responsible for taking care of the funds under NPS in the best interests of subscribers.

Pension Fund Regulatory and Development Authority (PFRDA) − An autonomous body set up by the Government of India to develop and regulate the pension market in India.

Public Provident Fund (PPF) Scheme

Public Provident Fund (PPF) is a 15-year investment scheme launched by government of India to enjoy a tax exempted investment. It was introduced by the National Savings Institute of the Ministry of Finance in 1968. A minimum yearly deposit of Rs. 500 is required to open and maintain a PPF account. It provides 7.9% interest. Loan facility is available in PPF account.

Bank on your mobile

Mobile plays a major role in day-to-day activities. We can access services provided by bank through mobile.

Mobile Banking

Mobile banking is a facility provided by all banks to make customers' work easy. Using mobile app, we can do the following activities.

Transfer funds from your account to another account.

Verify your bank account particulars.

Make payment of utility and credit card bills.

Open and renewal of fixed deposit account.

Recharge prepaid mobile/DTH.

Mobile Wallets

Mobile wallet is a virtual wallet, which stores your credit or debit card information. Instead of physically carrying card, we can use mobile device. Mobile wallet also helps to store driver's license, social security number, health information cards, loyalty cards, hotel key cards and bus or train tickets.

Summary

From this topic, we gained a detailed knowledge on the importance of savings; importance of bank, banking products like accounts, deposits, loans; procedure to open an account, banking services, ATM, internet banking, mobile banking, mobile wallet, insurance, and various schemes introduced by the Prime Minister of India.

To Continue Learning Please Login