- Time Series - Home

- Time Series - Introduction

- Time Series - Programming Languages

- Time Series - Python Libraries

- Data Processing & Visualization

- Time Series - Modeling

- Time Series - Parameter Calibration

- Time Series - Naive Methods

- Time Series - Auto Regression

- Time Series - Moving Average

- Time Series - ARIMA

- Time Series - Variations of ARIMA

- Time Series - Exponential Smoothing

- Time Series - Walk Forward Validation

- Time Series - Prophet Model

- Time Series - LSTM Model

- Time Series - Error Metrics

- Time Series - Applications

- Time Series - Further Scope

- Time Series Useful Resources

- Time Series - Quick Guide

- Time Series - Useful Resources

- Time Series - Discussion

Selected Reading

Time Series - Walk Forward Validation

In time series modelling, the predictions over time become less and less accurate and hence it is a more realistic approach to re-train the model with actual data as it gets available for further predictions. Since training of statistical models are not time consuming, walk-forward validation is the most preferred solution to get most accurate results.

Let us apply one step walk forward validation on our data and compare it with the results we got earlier.

In [333]:

prediction = [] data = train.values for t In test.values: model = (ExponentialSmoothing(data).fit()) y = model.predict() prediction.append(y[0]) data = numpy.append(data, t)

In [335]:

test_ = pandas.DataFrame(test) test_['predictionswf'] = prediction

In [341]:

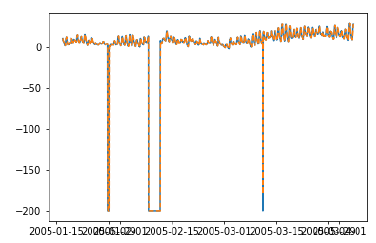

plt.plot(test_['T']) plt.plot(test_.predictionswf, '--') plt.show()

In [340]:

error = sqrt(metrics.mean_squared_error(test.values,prediction))

print ('Test RMSE for Triple Exponential Smoothing with Walk-Forward Validation: ', error)

Test RMSE for Triple Exponential Smoothing with Walk-Forward Validation: 11.787532205759442

We can see that our model performs significantly better now. In fact, the trend is followed so closely that on the plot predictions are overlapping with the actual values. You can try applying walk-forward validation on ARIMA models too.

Advertisements