Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

Selected Reading

Explain the different types of books of accounts

Books of accounts are defined as "a place where all financial information is related to a person or a business". Books of accounts are maintained under Income tax Act, companies Act 2013 and GST Act.

Maintaining books of accounts is compulsory if the turnover/gross receipts/sales from profession or business is above Rs.2500000/-. As per rule 6F, cash books, ledgers, bills/receipts (Bills), journals and daily cash registers come under books of accounts.

Types

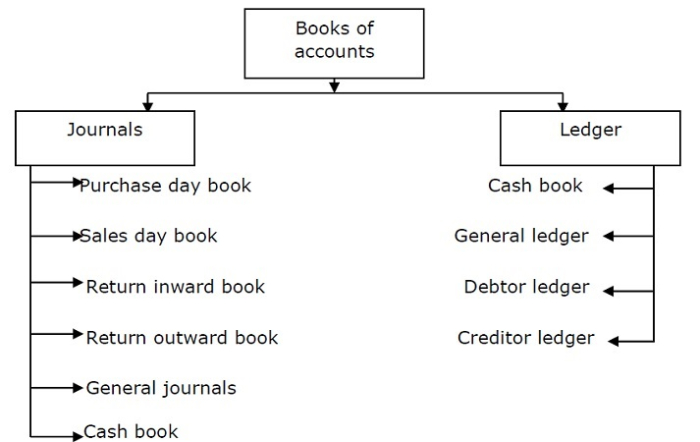

The two main types of the books of accounts are journal and ledger.

Journal is sub classified into the following −

- Purchase Day book − Original book of entry which records credit purchases is called purchase book/purchase day book.

- Sales Day book − Records the details of credit sales by businessmen.

- Return Inward book − It records returned goods by customer or goods returned to dealer/supplier by customer. It is also called a sales return book.

- Return outward book − It records goods returned to the supplier. This is also called a purchase return book.

- General journal − Records entries which do not fit in other books or miscellaneous transactions (credit).

- Cash book − This book records only cash receipts and payments related to cash.

Ledger is sub classified into the following −

- Cash book − only cash related receipts and payments are recorded.

- General ledger − All business financial transactions.

- Debtor ledger − Provides information about the credit sales (related to customers).

- Creditor ledger − Provides information about the credit purchases (related to sellers).

Updated on: 2022-05-13T07:38:27+05:30

26K+ Views

Advertisements