Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

Selected Reading

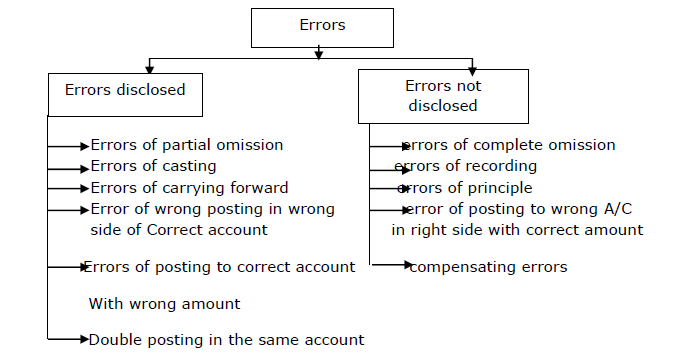

How are errors classified in trial balance?

Errors in trial balance are classified into two types namely, errors disclosed and errors not disclosed. Errors disclosed and errors not disclosed are again subdivided into several types.

Following diagram shows the classification of errors in trial balance −

Classification of errors based on nature

The classification of errors in trial balance which is based on nature is explained below:

Error of omission

- Error of complete omission

- Error of partial omission

Error of commission

- Error of recording in book of original entry

- Wrongly totaling of subsidiary book

- Error in balancing ledger accounts

- Error of posting − This is further classified as follows −

- Posting to the wrong side, but on the correct account.

- Posting with the wrong amount.

- Posting twice in the same account.

- Error in carrying forward.

Errors of principles

- Treating capital items as revenue items

- Treating revenue items as capital items

Compensating error

- Accounting error which offsets another accounting error

Updated on: 2022-05-18T09:49:54+05:30

459 Views

Advertisements