- XGBoost - Home

- XGBoost - Overview

- XGBoost - Architecture

- XGBoost - Installation

- XGBoost - Hyper-parameters

- XGBoost - Tuning with Hyper-parameters

- XGBoost - Using DMatrix

- XGBoost - Classification

- XGBoost - Regressor

- XGBoost - Regularization

- XGBoost - Learning to Rank

- XGBoost - Over-fitting Control

- XGBoost - Quantile Regression

- XGBoost - Bootstrapping Approach

- XGBoost - Python Implementation

- XGBoost vs Other Boosting Algorithms

- XGBoost Useful Resources

- XGBoost - Quick Guide

- XGBoost - Useful Resources

- XGBoost - Discussion

XGBoost - Bootstrapping Approach

The bootstrapping method can be combined with replaceable sampling to resample your data and produce many training sets. So, the bootstrapping strategy in XGBoost may be defined as a type of method where we train the model on many random subsets of the data to improve it.

How it works ?

An XGBoost model is trained for each resampled set and predictions are produced for the test data point. The distribution of these predictions provides a rough estimation of the predicted uncertainty.

So the bootstrapping strategy in XGBoost refers to a method of improving the model by training it on many random subsets of the data.

XGBoost generates a huge number of small models each of which is trained on a different portion of the available data. This type of random sampling is referred to as "bootstrapping". XGBoost combines the outputs of these small models and trains on various subsets of the data to produce a single, powerful prediction.

Using different random samples, this strategy attempts to reduce errors and improve model accuracy. It also helps the XGBoost model in avoiding overfitting, which occurs when a model performs well on training data but poorly on new data.

This is similar to how people learn by gaining new experiences.

Apply Bootstrapping to the Model

As we have seen in the bootstrapping method multiple models are trained using resampled versions of the training data, and their predictions are combined. The basic idea is to randomly select data, bootstrap multiple models, and then make predictions on test data that has not been seen before. By averaging the predictions and computing their variability, we can generate confidence intervals that show the degree of uncertainty in our predictions.

So let us see the steps to apply bootstrapping to the XGBoost model −

1. Importing Necessary Libraries and Generating Synthetic Data

First we will load the libraries like XGBoost, NumPy, and Matplotlib for training and analyzing the models. Next, we generate synthetic data to train the models.

# Importing libraries here import xgboost as xgb import numpy as np import matplotlib.pyplot as plt # Generate random training and testing data np.random.seed(123) X_train_data = np.random.rand(150, 8) y_train_target = np.random.rand(150) # Generate 30 samples with 8 features for testing X_test_data = np.random.rand(30, 8)

2. Bootstrapping

Now we will create multiple models by using the above bootstrapping method. Every time we randomly resample the training set, fit an XGBoost model to it and then make predictions about the test set. When we are trying to get a collection of predictions gathered from multiple bootstrapped datasets this method will be repeated multiple times.

# Number of bootstrapped models

n_iterations = 120

# List to store predictions from each model

all_preds = []

for iteration in range(n_iterations):

# Create a bootstrapped dataset

sampled_indices = np.random.choice(len(X_train_data), len(X_train_data), replace=True)

X_resampled_data, y_resampled_target = X_train_data[sampled_indices], y_train_target[sampled_indices]

# Initialize and train an XGBoost regression model

xgboost_model = xgb.XGBRegressor()

xgboost_model.fit(X_resampled_data, y_resampled_target)

# Make predictions on the test data

test_predictions = xgboost_model.predict(X_test_data)

all_preds.append(test_predictions)

# Convert the list of predictions to a NumPy array

all_preds = np.array(all_preds)

# Calculate the mean and standard deviation

avg_preds = np.mean(all_preds, axis=0)

std_dev_preds = np.std(all_preds, axis=0)

# Calculate 95% confidence intervals

lower_confidence_bound = avg_preds - 1.96 * std_dev_preds

upper_confidence_bound = avg_preds + 1.96 * std_dev_preds

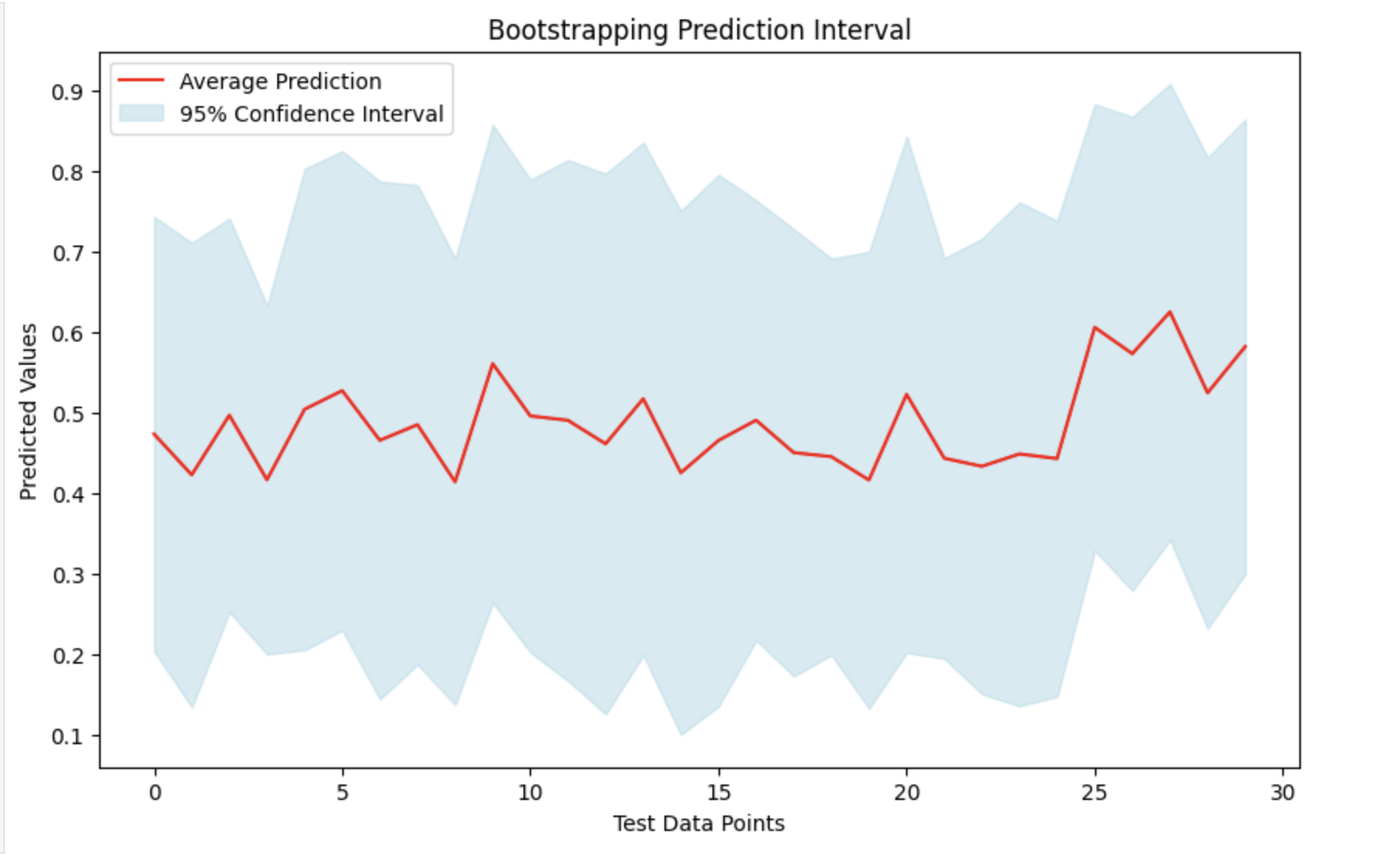

Visualize the Result

By taking the average (mean) of all the predictions and their standard deviations, we can create a prediction interval. This will help us to understand the range in which the actual figures will probably to fall and provides a measure of prediction uncertainty. We can see the findings by plotting the mean forecasts and highlighting the confidence interval around them.

# Visualization of the predictions with confidence intervals

# Set the figure size

plt.figure(figsize=(10, 6))

# Plot the mean predictions

plt.plot(avg_preds, label='Average Prediction', color='red')

# Fill the area between the lower and upper confidence bounds

plt.fill_between(range(len(avg_preds)), lower_confidence_bound, upper_confidence_bound, color='lightblue', alpha=0.5, label='95% Confidence Interval')

# Add title and labels to the plot

plt.title('Bootstrapping Prediction Interval')

plt.xlabel('Test Data Points')

plt.ylabel('Predicted Values')

# Add a legend to describe the plot lines

plt.legend()

# Display the plot

plt.show()

Output

This will produce the following result −