Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

Explain about Transfer pricing

In transfer pricing, the capital of one enterprise is used in another enterprise. That means management of one company can control another company. The main objectives are separate profits and performance is evaluated separately.

Secondly, it affects allocations of company resources. In this method cost incurred in one enterprise can be utilized in another enterprise.

The main purposes for transfer pricing are as follows −

- Direction of cash flows.

- Shifting profits.

- Minimize tax burden.

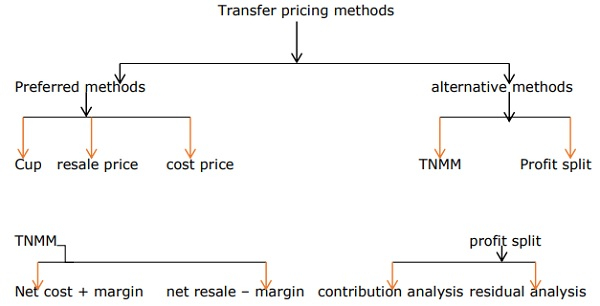

Methods of transfer pricing are as follows −

- Comparable uncontrolled price method.

- Resale price method or resale minus method.

- Cost plus method.

Arm's length principle

- Every country has its own taxation rules. It states that the terms and conditions for uncontrolled transactions are no different than for controlled transactions.

- Direct methods − In this, there is a comparison between prices/gross profits/normal gross profit margins.

- Indirect methods − It compares net profit margin/operating profit to a proper base. Here, profit is split into combined net profit and transactional net margin.

Requirements for transfer pricing are as follows −

- Proof that it follows the arm's length principle.

- Documentation of transfer pricing (establishment).

- File corporate taxes.

Transfer pricing Methods

These methods are explained below −

Cup method − compares terms & conditions, price of a transaction to 3rd party transactions.

Resale price − price where an associated enterprise sells a product to a 3rd party.

Cost price method − compares gross profits to cost of sales.

TNMM (Transactional net margin method) − determines net profit of controlled transactions of associated enterprises.

Profit split method − terms & conditions are examined by determining divisions of profits.

451 Views