- Foreign Exchange Markets

- Balance of Payments

- Forex Market Players

- International Capital Markets

- The Interest Rate Parity Model

- Monetary Assets

- Exchange Rates

- Interest Rates

- Forex Intervention

- International Money Market

- International Bond Markets

- International Equity Markets

- Hedging & Risk Management

- Exchange Rate Forecasts

- Exchange Rate Fluctuations

- Foreign Currency Futures & Options

- Transaction Exposure

- Translation Exposure

- Economic Exposure

- Strategic Decision Making

- Foreign Direct Investment

- Long-Term and Short-Term Financing

- Working Capital Management

- International Trade Finance

- International Finance Resources

- International Finance - Quick Guide

- International Finance - Resources

- International Finance - Discussion

International Finance - Quick Guide

International Finance - Introduction

International Finance is an important part of financial economics. It mainly discusses the issues related with monetary interactions of at least two or more countries. International finance is concerned with subjects such as exchange rates of currencies, monetary systems of the world, foreign direct investment (FDI), and other important issues associated with international financial management.

Like international trade and business, international finance exists due to the fact that economic activities of businesses, governments, and organizations get affected by the existence of nations. It is a known fact that countries often borrow and lend from each other. In such trades, many countries use their own currencies. Therefore, we must understand how the currencies compare with each other. Moreover, we should also have a good understanding of how these goods are paid for and what is the determining factor of the prices that the currencies trade at.

Note − The World Bank, the International Finance Corporation (IFC), the International Monetary Fund (IMF), and the National Bureau of Economic Research (NBER) are some of the notable international finance organizations.

International trade is one of the most important factors of growth and prosperity of participating economies. Its importance has got magnified many times due to globalization. Moreover, the resurgence of the US from being the biggest international creditor to become the largest international debtor is an important issue. These issues are a part of international macroeconomics, which is popularly known as international finance.

Importance of International Finance

International finance plays a critical role in international trade and inter-economy exchange of goods and services. It is important for a number of reasons, the most notable ones are listed here −

International finance is an important tool to find the exchange rates, compare inflation rates, get an idea about investing in international debt securities, ascertain the economic status of other countries and judge the foreign markets.

Exchange rates are very important in international finance, as they let us determine the relative values of currencies. International finance helps in calculating these rates.

Various economic factors help in making international investment decisions. Economic factors of economies help in determining whether or not investors money is safe with foreign debt securities.

Utilizing IFRS is an important factor for many stages of international finance. Financial statements made by the countries that have adopted IFRS are similar. It helps many countries to follow similar reporting systems.

IFRS system, which is a part of international finance, also helps in saving money by following the rules of reporting on a single accounting standard.

International finance has grown in stature due to globalization. It helps understand the basics of all international organizations and keeps the balance intact among them.

An international finance system maintains peace among the nations. Without a solid finance measure, all nations would work for their self-interest. International finance helps in keeping that issue at bay.

International finance organizations, such as IMF, the World Bank, etc., provide a mediators role in managing international finance disputes.

The very existence of an international financial system means that there are possibilities of international financial crises. This is where the study of international finance becomes very important. To know about the international financial crises, we have to understand the nature of the international financial system.

Without international finance, chances of conflicts and thereby, a resultant mess, is apparent. International finance helps keep international issues in a disciplined state.

International Financial Globalization

In the last two decades, the financial economies have increasingly got interconnected around the world. The impact of globalization has been felt in every aspect of economy. Financial globalization has offered substantial benefits to the national economies and to both investors and wealth creators. However, it has a wreaking effect on financial markets as well.

Driving Forces of Financial Globalization

When we talk about financial globalization, there are four major factors to be considered. They are −

Advancement in information and communication technologies − Technological advancements have made market players and governments far more efficient in collecting the information needed to manage financial risks.

Globalization of national economies − Economic globalization has made production, consumption, and investments dispersed over various geographic locations. As barriers to international trade have been lowered, international flows of goods and services have dramatically increased.

Liberalization of national financial and capital markets − Liberalization and fast improvements in IT and the globalization of national economies have resulted in highly spread financial innovations. It has increased the growth of international capital movements.

Competition among intermediary services providers − Competition has increased manifold due to technological advancements and financial liberalization. A new class of nonbank financial entities, including institutional investors, have also emerged.

Changes in Capital Markets

The driving forces of financial globalization have led to four dramatic changes in the structure of national and international capital markets.

First, banking systems have been under a process of disintermediation. Financial intermediation is happening more through tradable securities and not through bank loans and deposits.

Second, cross-border financing has increased. Investors are now trying to enhance their returns by diversifying their portfolios internationally. They are now seeking the best investment opportunities from around the world.

Third, the non-banking financial institutions are competing with banks in national and international markets, decreasing the prices of financial instruments. They are taking advantage of economies of scale.

Fourth, banks have accessed a market beyond their traditional businesses. It has enabled the banks to diversify their sources of income and the risks.

Benefits and Risks of Financial Globalization

One of the major benefits of Financial Globalization is that the risk of a "credit crunch" has been reduced to extremely low levels. When banks are under strain, they can now raise funds from international capital markets.

Another benefit is that, with more choices, borrowers and investors get a better pricing on their financing. Corporations can finance the investments more cheaply.

The disadvantage is that the markets are now extremely volatile, and this can be a threat to financial stability. Financial globalization has altered the balance of risks in international capital markets.

With financial globalization, creditworthy banks and businesses in emerging markets can now reduce their borrowing costs. However, emerging markets with weak or poorly managed banks are at risk.

Safeguarding Financial Stability

The crises of the 1990s have shown the importance for a prudent sovereign debt management, effective capital account liberalization, and management of domestic financial systems.

Private financial institutions and market players can now contribute to financial stability by managing their businesses well and avoiding unnecessary risk-taking.

As financial stability is a global public good, governments and regulators also play a key role in it. The scope of this role is increasingly getting international.

The IMF is a key role-player as well. Its global surveillance initiatives to enhance its ability to manage international financial stability must also stay in track.

Balance of Payments

It is important to measure the performance of an economy. Balance of Payment (BOP) is one way to do so. It shows the big picture of the total transactions of an economy with other economies. It takes the net inflows and outflows of money into account and then differentiates them into sections. It is important to balance all accounts of BOP in case of an imbalance so that the economic transactions can be measured and taken into account in a systematic and prudent manner.

Balance of Payment is a statement that shows an economys transactions with the remaining world in a given duration. Sometimes also called the balance of international payments, BOP includes each and every transaction between a nations residents and its nonresidents.

Current Account and Capital Account

All the transactions in BOP are classified into two accounts: the current account and the capital account.

Current account − It denotes the final net payment a nation is earning when it is in surplus, or spending when it is in deficit. It is obtained by adding the balance of trade (exports earnings minus imports expenses), factor income (foreign investment earning minus expenses for investment in a foreign country) and other cash transfers. The current word denotes that it covers transactions that are happening "here and now".

Capital account − It shows net change in foreign-asset-ownership of a nation. The capital account consists the reserve account (the net change of foreign exchange of a nation's central bank in market operations), loans and investments made by the nation (excluding the future interest payments and dividends yielded by loans and investments). If net foreign exchange is negative, the capital account is said to be in deficit.

BOP data does not include the real payments. Rather, it is involved with the transactions. This means that the figure of BOP may differ significantly from net payments made to an entity over a period of time.

BOP data is crucial in deciding the national and international economic policy. Part of the BOP, such as current account imbalances and foreign direct investment (FDI), are very important issues which are addressed in the economic policies of a nation. Economic policies with specific objectives impact the BOP.

The Tweak in Case of IMF

The IMF's BOP terminology uses the term "financial account" to include the transactions that would under alternative definitions be included in the general capital account. The IMF uses the term capital account for a subset of transactions that form a small part of the overall capital account. The IMF calculates the transactions in an additional top level division of the BOP accounts.

The BOP identity, according to IMF terminology, can be written as −

Current account + Financial account + Capital account + Balancing item = 0

According to IMF, the term current account has its own three leading sub-divisions, which are: the goods and services account (the overall trade balance), the primary income account (factor income), and the secondary income account (transfer payments).

Points to Note

BOP is an account to show the expenses made by consumers and firms on imported goods and services.

BOP is also a pointer to how much the successful firms of a country are exporting to foreign countries.

The money or the foreign currency entering a nation is taken as a positive entry (e.g. exports sold to foreign countries)

The money going out or expenses of foreign currency is adjusted as a negative entry (e.g. imports such as goods and services)

BOP Table for a Hypothetical Country

The following table shows the BOP for a hypothetical country.

| Item of the BoP | Net Balance ($ billion) | Comment |

|---|---|---|

| Current Account | ||

| (A) Balance of trade in goods | -20 | There is a trade deficit in goods. |

| (B) Balance of trade in services | +10 | There is a trade surplus in services. |

| (C) Net investment income | -12 | Net outflow of income, i.e., due to profits of international corporations |

| (D) Net overseas transfers | +8 | Net inflow of transfers, say, from remittances from non-resident citizens |

| Adding A+B+C+D = Current account balance | -14 | Overall, the nation runs a current account deficit |

| Financial Account | ||

| Net balance of FDI flows | +5 | Positive FDI net inflow |

| Net balance of portfolio investment flows | +2 | Positive net inflow into equity markets, property etc. |

| Net balance of short term banking flows | -2 | Small net outflow of currency from nations banking system |

| Balancing item | +2 | There to reflect errors and omissions in data calculations |

| Changes to reserves of gold and foreign currency | +7 | (Means that gold and foreign currency reserves have been reduced |

| Overall balance of payments | 0 | |

BOP Imbalances

BOP has to balance, however surpluses or deficits on its individual elements may create imbalances. There are concerns about deficits in the current account. The types of deficits that typically raise concerns are −

A visible trade deficit in case of a nation that is importing significantly more goods than it exports.

An overall current account deficit.

A basic deficit which is the current account plus FDI, excluding short-term loans and the reserve account.

Reasons behind BOP Imbalances

Conventionally, current accounts factors are thought to be the primary cause behind BOP imbalances these include the exchange rate, the fiscal deficit, business competitiveness, and private behavior.

Alternatively, it is believed that the capital account is the major driver of imbalances where a global savings satiation created by the savers in surplus countries goes ahead of the present investment opportunities.

Reserve Assets

BOP defines the reserve asset as the currency or other standard value that is used for their foreign reserves. The reserve asset can either be gold or the US Dollar.

Global Reserves

According to IMF, between 2000 to mid-2009, official reserves increased from $1,900 billion to $6,800 billion. Global reserves were at the top, about $7,500 billion in mid-2008, then the reserves declined by about $430 billion during the financial crisis. From Feb 2009, global reserves increased again to reach $9,200 billion by the end of 2010.

BOP Crisis

A BOP crisis, or currency crisis, is the inability of a nation to pay for the necessary imports and/or return the pending debts. Such a crisis occurs with a very quick decline of the nation's currency value. Crises are generally preceded by large capital inflows.

How to Correct BOP Imbalances

There are three possible processes to correct BOP imbalances −

- Adjustments of exchange rates,

- Adjustment of nations internal prices along with its levels of demand, and

- Rules-based adjustment.

Rebalancing by Changing the Exchange Rate

If a nation's currency price is increased, it will make exports less competitive and imports cheaper.

When a country is exporting more than what it imports, the demand for its currency will increase in foreign countries because other countries ultimately seek the country's currency to pay for the exports. Therefore, if the country is earning more, it will change (increase) the exchange rate to contain the current account surplus.

Rebalancing by Adjusting Internal Prices and Demand

A possible policy is to increase its level of internal demand (i.e. the nations expenditure on goods). An alternative expression for current account is that it is the excess of savings over investment. That is,

Current Account = National Savings National Investment

When the Savings are in surplus, the nation can increase its investments. For example, in 2009, Germany amended its constitution to reduce its surplus by increasing demand.

Rules-based rebalancing mechanisms

Nations can also agree to determine the exchange rates against each other, and then try to correct the imbalances by rules-based and mutually negotiated exchange-rate changes.

The Bretton Woods system of fixed but adjustable exchange rates is an example of a rules-based system.

Keynesian Idea for Rules-based Rebalancing

John Maynard Keynes believed that surpluses impose negative effects on the global economy. He suggested that traditional balancing mechanisms should add the threat of possession of a section of excess revenue if the surplus country chooses not to spend it on additional imports.

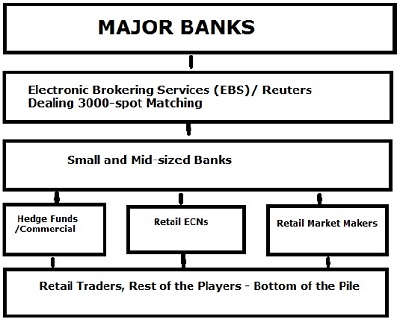

Forex Market Players

There are various players in the Foreign Exchange (Forex) market and all of them are important in one way or the other. In this chapter, we take each one of them and check their major attributes and responsibilities in the overall Forex market.

Interestingly, internet technology has really changed the existence and working policies of the Forex market-players. These players now have easier access to data and are more productive and prompt in offering their respective services.

Capitalization and sophistication are two major factors in categorizing the Forex market players. The sophistication factor includes money management techniques, technological level, research abilities, and the level of discipline. Considering these two broad measures, there are six major Forex market players −

- Commercial and Investment Banks

- Central Banks

- Businesses and Corporations

- Fund Managers, Hedge Funds, and Sovereign Wealth Funds

- Internet-based Trading Platforms

- Online Retail Broker-Dealers

The following figure depicts the top-to-bottom segmentation of Foreign Exchange Market players in terms of the volume they handle in the market.

Commercial and Investment Banks

Banks need no introduction; they are ubiquitous and numerous. Their role is crucial in the Forex network. The banks take part in the currency markets to neutralize the foreign exchange risks of their own and that of their clients. The banks also seek to multiply the wealth of their stockholders.

Each bank is different in terms of its organization and working policy, but each one of them has a dealing desk responsible for order processing, market-making, and risk management. The dealing desk plays a role in making profits by trading currency straight through hedging, arbitrage, or a mixed array of financial strategies.

There are many types of banks in a forex market; they can be huge or small. The most sizeable banks deal in huge amounts of funds that are being traded at any instant. It is a common standard for banks to trade in 5 to 10 million Dollar parcels. The biggest ones even handle 100 to 500 million Dollar parcels.

Central Banks

A central bank is the predominant monetary authority of a nation. Central banks obey individual economic policies. They are usually under the authority of the government. They facilitate the governments monetary policies (dealing in keeping the supply and the availability of money) and to make strategies to smoothen out the ups and downs of the value of their currency.

We have earlier discussed about the reserve assets. Central banks are the bodies responsible for holding the foreign currency deposits called "reserves" aka "official reserves" or "international reserves".

The reserves held by the central banks of a country are used in dealing with foreign-relation policies. The reserves value indicates significant attributes about a countrys ability to service foreign debts; it also affects the credit rating measures of the nation.

Businesses and Corporations

All participants involved in the forex market do not have the power to set prices of the currency as market makers. Some of the players just buy and sell currency following the prevailing exchange rate. They may seem to be not so significant, but they make up a sizeable allotment of the total volume that is being traded in the market.

There are companies and businesses of differing sizes; they may be a small importer/exporter or a palpable influencer with a multi-billion Dollar cash flow capability. These players are identified by the nature of their business policies that include: (a) how they get or pay for the goods or services they usually render and (b) how they involve themselves in business or capital transactions that require them to either buy or sell foreign currency.

These "commercial traders" have the aim to utilize financial markets to offset their risks and hedge their operations. There are some non-commercial traders as well. Unlike commercial traders, the non-commercial ones are considered speculators. Non-commercial players include large institutional investors, hedge funds, and other business entities that trade in the financial markets for profits.

Fund Managers, Hedge Funds, and Sovereign Wealth Funds

This category is not involved in defining the prices or controlling them. They are basically transnational and home-countrys money managers. They may deal in hundreds of millions of dollars, as their portfolios of investment funds are often quite large.

These participants have investment charters and obligations to their investors. The major aim of hedge funds is to make profits and grow their portfolios. They want to achieve absolute returns from the Forex market and dilute their risk. Liquidity, leverage, and low cost of creating an investment environment are the advantages of hedge funds.

Fund managers mainly invest on behalf of the various clients they have, such as the pension funds, individual investors, governments and even the central bank authorities. Sovereign wealth funds that manage government-sponsored investment pools have grown at a fast rate in the recent years.

Internet-based Trading Platforms

Internet is an impersonal part of the forex markets nowadays. Internet-based trading platforms do the task of systematizing customer/order matching. These platforms are responsible for being a direct access point to accumulate pools of liquidity.

There is also a human element in the brokering process. It includes all the people engaged from the instant an order is put to the trading system till it is dealt and matched by a counter party. This category is being handled by the "straight-through-processing" (STP) technology.

Like the prices of a Forex broker's platform, a lot of inter-bank deals are now being handled electronically by two primary platforms: the Reuters web-based dealing system, and the Icap's EBS which is short for "electronic brokering system that replace the voice broker once common in the foreign exchange markets.

Online Retail Broker-Dealers

The last segment of the Forex markets, the brokers, are usually very huge companies with huge trading turnovers. This turnover provides the basic infrastructure to the common individual investors to invest and profit in the interbank market. Most of the brokers are taken to be a market maker for the retail trader. To provide competitive and popular two-way pricing model, these brokers usually adapt to the technological changes available in the Forex industry.

A trader needs to produce gains independently while using a market maker or having a convenient and direct access through an ECN.

The Forex broker-dealers offset their positions in the interbank market, but they do not act exactly the same way as banks do. Forex brokers do not rely on trading platforms like EBS or Reuters Dealing. Instead, they have their own data feed that supports their pricing engines.

Brokers typically need a certain pool of capitalization, legal business agreements, and straightforward electronic contacts with one or multiple banks.

The Interest Rate Parity Model

What is Interest Rate Parity?

Interest Rate Parity (IRP) is a theory in which the differential between the interest rates of two countries remains equal to the differential calculated by using the forward exchange rate and the spot exchange rate techniques. Interest rate parity connects interest, spot exchange, and foreign exchange rates. It plays a crucial role in Forex markets.

IRP theory comes handy in analyzing the relationship between the spot rate and a relevant forward (future) rate of currencies. According to this theory, there will be no arbitrage in interest rate differentials between two different currencies and the differential will be reflected in the discount or premium for the forward exchange rate on the foreign exchange.

The theory also stresses on the fact that the size of the forward premium or discount on a foreign currency is equal to the difference between the spot and forward interest rates of the countries in comparison.

Example

Let us consider investing € 1000 for 1 year. We'll have two options as investment cases −

Case I: Home Investment

In the US, let the spot exchange rate be $1.2245 / €1.

So, practically, we get an exchange for our €1000 @ $1.2245 = $1224.50

We can invest this money $1224.50 at the rate of 3% for 1 year which yields $1261.79 at the end of the year.

Case II: International Investment

We can also invest €1000 in an international market, where the rate of interest is 5.0% for 1 year.

So, €1000 @ of 5% for 1 year = €1051.27

Let the forward exchange rate be $1.20025 / €1.

So, we buy forward 1 year in the future exchange rate at $1.20025/€1 since we need to convert our €1000 back to the domestic currency, i.e., the U.S. Dollar.

Then, we can convert € 1051.27 @ $1.20025 = $1261.79

Thus, when there is no arbitrage, the Return on Investment (ROI) is equal in both cases, regardless the choice of investment method.

Arbitrage is the activity of purchasing shares or currency in one financial market and selling it at a premium (profit) in another.

Covered Interest Rate Parity (CIRP)

According to Covered Interest Rate theory, the exchange rate forward premiums (discounts) nullify the interest rate differentials between two sovereigns. In other words, covered interest rate theory says that the difference between interest rates in two countries is nullified by the spot/forward currency premiums so that the investors could not earn an arbitrage profit.

Example

Assume Yahoo Inc., the U.S. based multinational, has to pay the European employees in Euro in a month's time. Yahoo Inc. can do this in many ways, one of which is given below −

Yahoo can buy Euro forward a month (30 days) to lock in the exchange rate. Then it can invest this money in dollars for 30 days after which it must convert the dollars to Euro. This is known as covering, as now Yahoo Inc. will have no exchange rate fluctuation risk.

Yahoo can also convert the dollars to Euro now at the spot exchange rate. Then it can invest the Euro money it has obtained in a European bond (in Euro) for 1 month (which will have an equivalently loan of Euro for 30 days). Then Yahoo can pay the obligation in Euro after one month.

Under this model, if Yahoo Inc. is sure that it will earn an interest, it may convert fewer dollars to Euro today. The reason for this being the Euros growth via interest earned. It is also known as covering because by converting the dollars to Euro at the spot rate, Yahoo is eliminating the risk of exchange rate fluctuation.

Uncovered Interest Rate Parity (UIP)

Uncovered Interest Rate theory says that the expected appreciation (or depreciation) of a particular currency is nullified by lower (or higher) interest.

Example

In the given example of covered interest rate, the other method that Yahoo Inc. can implement is to invest the money in dollars and change it for Euro at the time of payment after one month.

This method is known as uncovered, as the risk of exchange rate fluctuation is imminent in such transactions.

Covered Interest Rate and Uncovered Interest Rate

Contemporary empirical analysts confirm that the uncovered interest rate parity theory is not prevalent. However, the violations are not as huge as previously contemplated. The violations are in the currency domain rather than being time horizon dependent.

In contrast, the covered interest rate parity is an accepted theory in recent times amongst the OECD economies, mainly for short-term investments. The apparent deviations incurred in such models are actually credited to the transaction costs.

Implications of IRP Theory

If IRP theory holds, then it can negate the possibility of arbitrage. It means that even if investors invest in domestic or foreign currency, the ROI will be the same as if the investor had originally invested in the domestic currency.

When domestic interest rate is below foreign interest rates, the foreign currency must trade at a forward discount. This is applicable for prevention of foreign currency arbitrage.

If a foreign currency does not have a forward discount or when the forward discount is not large enough to offset the interest rate advantage, arbitrage opportunity is available for the domestic investors. So, domestic investors can sometimes benefit from foreign investment.

When domestic rates exceed foreign interest rates, the foreign currency must trade at a forward premium. This is again to offset prevention of domestic country arbitrage.

When the foreign currency does not have a forward premium or when the forward premium is not large enough to nullify the domestic country advantage, an arbitrage opportunity will be available for the foreign investors. So, the foreign investors can gain profit by investing in the domestic market.

International Finance - Monetary Assets

Monetary assets are cash in possession of a corporation, country, or a company. There is always some demand and an equivalent amount of supply for each countrys currency. The cash in hand determines the strength of an economy.

Monetary assets have a dollar value that will not change with time. These assets have a constant numerical value. For example, a dollar is always a dollar. The numbers will not change even if the purchasing power of the currency changes.

We can understand this concept by contrasting them against a non-monetary item like a production facility. A production facilitys value its price denoted by a number of dollars may fluctuate in future. It may lose or gain value over the years. So a company owning the factory may record the factory as being worth $500,000 one year and $480,000 the next. But, if the company has $500,000 in cash, it will be recorded as $500,000 every year.

In other words, monetary items are just cash. It can be a debt owed by an entity, a debt owed to it, or a cash reserve in its account.

For example, if a company owes $40,000 for goods delivered by a supplier. It will be recorded at $40,000 three months later even though, the company may have to pay $3,000 more because of inflation.

Similarly, if a company has $300,000 in cash, that $300,000 is a monetary asset and will be recorded as $300,000 even when, five years later, it may be able to only buy $280,000 worth of goods compared to when it was first recorded five years ago.

Demand and Supply of Currency in Forex Market

The demand for currencies in forex markets arise from the demand for a countrys exports. Also, speculators who are looking for a profit relying on the changes in currency values create demand.

The supply of a particular currency is derived by domestic demands for imports from the foreign nations. For example, let us suppose the UK has imported some cars from Japan. So, UK must pay the price of cars in Yen (), and it will have to buy Yen. To buy Yen, it must sell (supply) Pounds. The more the imports, the greater will be the supply of Pounds onto the Forex market.

International Finance - Exchange Rates

Due to demand and supply, there is always an exchange rate that keeps changing over time. The rate of exchange is the price of one currency expressed in terms of another. Due to increased or decreased demand, the currency of a country always has to maintain an exchange rate. The more the exchange rate, the more is the demand of that currency in forex markets.

Exchanging the currencies refer to trading of one currency for another. The value at which an exchange of currencies takes place is known as the exchange rate. The exchange rate can be regarded as the price of one particular currency expressed in terms of the other one, such as 1 (GBP) exchanging for US$1.50 cents.

The equilibrium between supply and demand of currencies is known as the equilibrium exchange rate.

Example

Let us assume that both France and the UK produce goods for each other. They will naturally wish to trade with each other. However, the French producers will have to pay in Euros and the British producers in Pounds Sterling. However, to meet their production costs, both need payment in their own local currency. These needs are met by the forex market which enables both French and British producers to exchange currencies so that they can trade with each other.

The market usually creates an equilibrium rate for each currency, which will exist where demand and supply of currencies intersect.

Changes in Exchange Rates

Changes in currency exchange rate may occur due to changes in demand and supply. In case of a demand and supply graph, the price of a currency, say Sterling, is expressed in terms of another currency, such as the $US.

When exports increase, it would shift the demand curve for Sterling to the right and the exchange rate will go up. One Pound was bought at $1.50, but now it buys $1.60, hence the value has gone up.

Note − The worlds three most common currency transactions are exchanges between the Dollar and the Euro (30%), the Dollar and the Yen (20%), and the Dollar and the Pound Sterling (12%).

International Finance - Interest Rates

Each currency carries an interest rate. It is like a barometer of the strength or weakness of an economy. If a countrys economy strengthens, the prices may sometime rise due to the fact that the consumers become able to pay more. This may sometimes result in a situation where more money is spent for roughly the same goods. This can increase the price of the goods.

When inflation goes uncontrolled, the moneys buying power decreases, and the price of ordinary items may rise to unbelievably high levels. To stop this imminent danger, the central bank usually raises the interest rates.

When the interest rate is increased, it makes the borrowed money more expensive. This, in turn, demotivates the consumers from buying new products and incurring additional debts. It also discourages the companies from expansion. The companies that do business on credit have to pay interest, and hence they do not spend too much in expansion.

The higher rates will gradually slow the economies down, until a point of saturation will come where the Central Bank will have to lower the interest rates. This reduction in rates is aimed at encouraging the economic growth and expansion.

When the interest rate is high, foreign investors desire to invest in that economy to earn more in returns. Consequently, the demand for that currency increases as more investors invest there.

Countries offering the highest RoI by offering high interest rates tend to attract heavy foreign investments. When a country's stock exchange is doing well and offer a good interest rate, the foreign investors are encouraged to invest capital in that country. This again increases the demand for the countrys currency, and value of the currency rises.

In fact, it is not just the interest rate that is important. The direction of movement of the interest rate is a good pointer of demand of the currency.

International Finance - Forex Intervention

Foreign exchange intervention is a monetary policy of a nations central bank. It is aimed at controlling the foreign exchange rates so that the interest rates and thereby the inflation in the country is kept under control.

Many developed countries nowadays believe in non-intervention. It has been backed by research that intervention may not be a good policy for the developed economies. However, the recession has again brought the topic under consideration as whether Forex intervention is really necessary to keep the economy affluent.

Foreign exchange intervention is an intervention of the central bank of a nation to influence the monetary funds-transfer rate of the national currency. Central banks generally intervene in the Forex market to increase the reserves, stabilize the fluctuating exchange rate and rectify misalignments. The success of intervention depends on the sterilization of the impact, and the general government macroeconomic policies.

There are mainly two difficulties in an intervention process. They are the determination of the timing and the amount. These decisions are often a judgment and not a set policy. The reserve capacity, the countrys exact type of economic troubles, and its fluctuating market conditions affect the decision-making process.

Forex interventions can be risky because it can degrade the central bank's credibility in case of a failure.

Why Forex Intervention?

The primary objective of Forex intervention is to adjust the volatility or to change the level of the exchange rate. Excessive short-term volatility diminishes market confidence and affects both the financial and the real goods markets.

In case of instability, exchange rate uncertainty results in extra costs and reduction of profits for companies. Investors do not invest in foreign financial assets and firms do not trade internationally. Exchange rate fluctuation affects the financial markets and thereby threatens the financial system. The governments monetary policy goals become more difficult to attain. In such situations, intervention is necessary.

Moreover, during change of economic condition and when the market misinterprets the economic signals, foreign exchange intervention rectifies the rates so that overshooting can be avoided.

Non-intervention

Today, forex market intervention is hardly used in developed countries. The reasons for non-intervention are −

Intervention is only effective when seen as preceding interest rate or other similar policy adjustments.

Intervention has no lasting impact on the real exchange rate and thus on competitive factors for the tradable sector.

Large-scale intervention diminishes the effectiveness of monetary policy.

Private markets can absorb and manage enough shocks guiding is unnecessary.

Direct Intervention

Direct currency intervention is generally defined as foreign exchange transactions that are conducted by the monetary authority and aimed at influencing the exchange rate. Depending on the monetary base changes, currency intervention can be broadly divided into two types: sterilized and non-sterilized interventions.

Sterilized intervention

Sterilized intervention influences the exchange rate without changing the monetary base. There are two steps in it. First, the central bank buys (selling) foreign currency bonds with domestic currency. Then the monetary base is sterilized by selling (buying) equivalent domestic-currency-denominated bonds.

The net effect is the same as a swap of domestic bonds for foreign bonds without money supply changes. The purchase of foreign exchange is accompanied by a sale of an equivalent amount of domestic bonds, and vice versa.

The sterilized intervention has little or no effect on domestic interest rates. However, sterilized intervention can influence the exchange rate through the following two channels −

The Portfolio Balance Channel − In the portfolio balance approach, agents balance their portfolios of domestic currency and bonds, and foreign currency and bonds. In case of any change, a new equilibrium is reached by changing the portfolios. Portfolio balancing influences the exchange rates.

The Expectations or Signalling Channel − According to the signalling channel theory, agents see exchange rate intervention as a signal for a change of policy. The change of expectation affects the current level of the exchange rate.

Non-sterilized intervention

Non-sterilized intervention affects the monetary base. The exchange rate is affected due to purchase or sale of foreign money or bonds with domestic currency.

In general, non-sterilization influences the exchange rate by bringing changes in the monetary base stock, which, in turn, changes the monetary assets, interest rates, market expectations and finally, the exchange rate.

Indirect intervention

Capital controls (taxing international transactions) and exchange controls (restricting trade in currencies) are indirect interventions. Indirect intervention influences the exchange rate indirectly.

Chinese Yuan Devaluation

There had been a large increase in American imports of Chinese goods in the 1990s and 2000s. Chinas central bank allegedly devalued Yuan by buying large amounts of US dollars. This has increased the supply of the Yuan in the market, and also increased the demand for US dollars, increasing the Dollar price.

At the end of 2012, China had a reserve of $3.3 trillion, which is the highest foreign exchange reserve in the world. Roughly, 60% of this reserve is US government bonds and debentures.

The actual effects of the devalued Yuan on capital markets, trade deficits, and the US domestic economy are highly debated. It is believed that the Yuan devaluation helps China as it boosts its exports, but hurts the United States by widening its trade deficit. It has been suggested that the US should apply tariffs on Chinese goods.

Another viewpoint is that US protectionism may hurt the US economy. Many think the undervalued Yuan hurts China more in the long-run, as a devalued Yuan doesnt subsidize the Chinese exporter, but subsidizes the American importer. Thus, they argue that importers within China have been substantially hurt due to the large-scale foreign exchange intervention.

International Money Market

A money market is one of the safest financial markets available for currency transactions. It is often used by the big financial institutions, large corporations, and national governments. The investments made in money markets are usually for a very short period of time and therefore they are commonly known as cash investments.

The International Money Market

The international money market is a market where international currency transactions between numerous central banks of countries are carried on. The transactions are mainly carried out using gold or in US dollar as a base. The basic operations of the international money market include the money borrowed or lent by the governments or the large financial institutions.

The international money market is governed by the transnational monetary transaction policies of various nations currencies. The international money markets major responsibility is to handle the currency trading between the countries. This process of trading a countrys currency with another one is also known as forex trading.

Unlike share markets, the international money market sees very large funds transfer. The players of the market are not individuals; they are very big financial institutions. The international money market investments are less risky and consequently, the returns obtained from the investments are less too. The best and most popular investment method in the international money market is via money market mutual funds or treasury bills.

Note − The international money market handles huge sums of international currency trading on a daily basis. The Bank for International Settlements has revealed that the daily turnover of a traditional exchange market is about $1880 billion.

Some of the major international money market participants are −

- Citigroup

- Deutsche Bank

- HSBC

- Barclays Capital

- UBS AG

- Royal Bank of Scotland

- Bank of America

- Goldman Sachs

- Merrill Lynch

- JP Morgan Chase

The international money market keeps track of the exchange rates between currency- pairs on a regular basis. Currency bands, fixed exchange rate, exchange rate regime, linked exchange rates, and floating exchange rates are the common indices that govern the international money market in a subtle manner.

The International Monetary Market

The International Monetary Market (IMM) was formed in December 1971 and was established in May 1972. The roots of IMM can be linked to the finish of Bretton Woods via the 1971 Smithsonian Agreement and then, Nixon's abolition of US dollar's convertibility to gold.

The IMM was formed as a separate entity of the Chicago Mercantile Exchange (CME). By the end of 2009, IMM was the second biggest futures exchange in terms of currency volume in the world. The major purpose of the IMM is to trade currency futures. It is comparatively a new product which was earlier studied by the academics as a tool to operate a freely-traded exchange market to initiate trade among the nations.

The first futures transactions included trades of currencies against the US dollar, such as the British Pound, Swiss Franc, German Deutschmark, Canadian Dollar, Japanese Yen, and the French Franc. The Australian Dollar, the Euro, emerging market currencies such as the Russian Ruble, Brazilian Real, Turkish Lira, Hungarian Forint, Polish Zloty, Mexican Peso, and South African Rand were later introduced as well.

The Drawbacks of Currency Futures

The challenge of the IMM was in connecting the values of IMM foreign exchange contracts to the interbank market, which is the prominent means of currency trading in the 1970s. The other aspect was how to allow the IMM to become the best and a free-floating exchange.

To contain these aspects, clearing member-firms were allowed to act as the arbitrageurs between central banks and the IMM to allow orderly markets between the bid and ask spreads.

Later on, the Continental Bank of Chicago was incorporated as a delivery agent for contracts. These initial successes led to fierce competition for new futures products.

The Chicago Board Options Exchange was a competitor. It had received the right to trade US 30-year bond futures while the IMM obtained the official right to trade Eurodollar contracts. The Eurodollars were a 90-day interest rate contract settled in cash and not in any physical delivery.

Eurodollars later became the "Eurocurrency Market," which were mainly used by the Organization for Petroleum Exporting Countries (OPEC). OPEC required payment for oil in US dollars.

This cash settlement aspect later introduced index futures known as IMM Index. Cash settlements also allowed the IMM to later known as a "cash market" because the trades were interest rate sensitive instruments of short-term.

A System for Transactions

As competition grew, a transaction-system to handle the transactions in IMM was required. The CME and Reuters Holdings introduced Post Market Trade (PMT) for worldwide electronic automated transactions. The system became the single clearing entity to link the major financial centres like Tokyo and London.

Now, PMT is called Globex, which deals not only in clearing but also in electronic trading for traders around the world. In 1976, US T-bills began trading on the IMM. T-bill futures were introduced in April 1986 that was approved by the Commodities Futures Trading Commission.

Financial Crises and Liquidity

In financial crises, central banks need to provide liquidity to stabilize markets, as risks may trade at premiums (money rates) to a bank's target rates. Central bankers then need to infuse liquidity to the banks that trade and control rates. These are known as repo rates, and these are traded via IMM.

Repo markets allow the participating banks to offer rapid refinancing in the interbank market that is independent of any credit limits to smoothen the market.

A borrower has to pledge for securitized assets, such as equity, in exchange for cash to allow its operations to continue.

International Bond Markets

Unlike Equity and Money markets, there is no specific bond market to trade bonds. However, there are domestic and foreign participants who sell and buy bonds in various bond markets.

A bond market is much larger than equity markets, and the investments are huge too. However, bonds pay on maturity and they are traded for short-time before maturity in the markets.

Bonds also have risks, returns, indices, and volatility factors like equity and money markets. The international bond market is composed of three separate types of bond markets: Domestic Bonds, Foreign Bonds, and Eurobonds.

Domestic Bonds

Domestic bonds trade is a part of the international bond market. Domestic bonds are dealt in local basis and domestic borrowers issue the local bonds. Domestic bonds are bought and sold in local currency.

Foreign Bonds

In foreign bond market, bonds are issued by foreign borrowers. Foreign bonds normally use the local currency. The concerned local market authorities supervise the issuance and sale of foreign bonds.

Foreign bonds are traded in the foreign bond markets. Some special characteristics of the foreign bond markets are −

- Issuers of bonds are usually governments and private sector utilities.

- It is a standard practice to underwrite and organize underwriting the risks.

- Issues are generally pledged by the retail and the institutional investors.

In the past, Continental private banks and old merchant houses in London linked the investors with the issuers.

Eurobonds

Eurobonds are not sold in any specific national bond market. A group of multinational banks issue Eurobonds. A Eurobond of any currency is sold outside the nation that has the currency. A Eurobond in the US dollar would not be sold in the United States.

The Euromarket is the trading place of Eurobonds, Eurocurrency, Euronotes, Eurocommercial Papers, and Euroequity. It is commonly an offshore market.

International Bond market participants

Bond market participants are either buyers (debt issuer) or sellers (institution) of funds and often both of these. Participants include −

- Institutional investors

- Governments

- Traders

- Individuals

Since there is a specificity of individual bond issues, and a condition of lack of liquidity in case of many smaller issues, a significantly larger chunk of outstanding bonds are often held by institutions, such as pension funds, banks, and mutual funds. In the United States, the private individuals own about 10% of the market.

International Bond Market Size

Amounts outstanding on the global bond market on March 2012 were about $100 trillion. That means in March 2012, the bond market was much larger than the global equity market that accounted for a market capitalization of around $53 trillion.

The outstanding value of international bonds in 2011 was about $30 trillion. There was a total issuance of $1.2 trillion in the year, which was down by around one fifth of the 2010s total. In 2012, the first half saw a strong start with issuance of over $800 billion.

International Bond Market Volatility

For the market participants owning bonds, collecting coupons and holding it till maturity, market volatility is not a matter to ponder over. The principal and interest rates are pre-determined for them.

However, participants who trade bonds before maturity face many risks, including the most important one changes in interest rates. When interest rates increase, the bond-value falls. Therefore, changes in bond prices are inversely proportional to the changes in interest rates.

Economic indicators and paring with actual data usually contribute to market volatility. Only little price movement is seen after the release of "in-line" data. When economic release does not match the consensus view, a rapid price movement is seen in the market. Uncertainty is responsible for more volatility.

Bond Investments

Bonds have (generally) $1,000 increments. Bonds are priced as a percentage of par value. Many bonds have minimums imposed on them.

Bonds pay interests at given intervals. Bonds with fixed coupons usually divide the coupon according to the payment schedule. Bonds with floating rate coupons have set calculation schedules. The rate is calculated just before the next payment. Zero-coupon bonds are issued at a deep discount, but they dont pay interests.

Bond interest is taxed, but in contrast to dividend income that receives favorable taxation rates, they are taxed as ordinary. Many government bonds are, however, exempt from taxation.

Individual investors can participate through bond funds, closed-end funds, and unit-investment trusts offered by investment companies.

Bond Indices

A number of bond indices exist. The common American benchmarks include Barclays Capital Aggregate Bond Index, Citigroup BIG, and Merrill Lynch Domestic Master.

International Equity Markets

International equity markets are an important platform for global finance. They not only ensure the participation of a wide variety of participants but also offer global economies to prosper.

To understand the importance of international equity markets, market valuations and turnovers are important tools. Moreover, we must also learn how these markets are composed and the elements that govern them. Cross-listing, Yankee stocks, ADRs and GRS are important elements of equity markets.

In this chapter, we will discuss all these aspects along with the returns from international equity markets.

Market Structure, Trading Practices, and Costs

The secondary equity markets provide marketability and share valuation. Investors or traders who purchase shares from the issuing company in the primary market may not desire to own them forever. The secondary market permits the shareholders to reduce the ownership of unwanted shares and lets the purchasers to buy the stock.

The secondary market consists of brokers who represent the public buyers and sellers. There are two kinds of orders −

Market order − A market order is traded at the best price available in the market, which is the market price.

Limit order − A limit order is held in a limit order book until the desired price is obtained.

There are many different designs for secondary markets. A secondary market is structured as a dealer market or an agency market.

In a dealer market, the broker takes the trade through the dealer. Public traders do not directly trade with one another in a dealer market. The over-the-counter (OTC) market is a dealer market.

In an agency market, the broker gets clients orders via an agent.

Not all stock market systems provide continuous trading. For example, the Paris Bourse was traditionally a call market where an agent gathers a batch of orders that are periodically executed throughout the trading day. The major disadvantage of a call market is that the traders do not know the bid and ask quotations prior to the call.

Crowd trading is a form of non-continuous trade. In crowd trading, in a trading ring, an agent periodically announces the issue. The traders then announce their bid and ask prices, and look for counterparts to a trade. Unlike a call market which has a common price for all trades, several trades may occur at different prices.

Trading In International Equities

A greater global integration of capital markets became apparent for various reasons −

First, investors understood the good effects of international trade.

Second, the prominent capital markets got more liberalized through the elimination of fixed trading commissions.

Third, internet and information and communication technology facilitated efficient and fair trading in international stocks.

Fourth, the MNCs understood the advantages of sourcing new capital internationally.

Cross-listing

Cross-listing refers to having the shares listed on one or more foreign exchanges. In particular, MNCs do this generally, but non-MNCs also cross-list. A firm may decide to cross-list its shares for the following reasons −

Cross-listing provides a way to expand the investors base, thus potentially increasing its demand in a new market.

Cross-listing offers recognition of the company in a new capital market, thus allowing the firm to source new equity or debt capital from local investors.

Cross-listing offers more investors. International portfolio diversification is possible for investors when they trade on their own stock exchange.

Cross-listing may be seen as a signal to investors that improved corporate governance is imminent.

Cross-listing diminishes the probability of a hostile takeover of the firm via the broader investor base formed for the firms shares.

Yankee Stock Offerings

In 1990s, many international companies, including the Latin Americans, have listed their stocks on U.S. exchanges to prime market for future Yankee stock offerings, that is, the direct sale of new equity capital to U.S. public investors. One of the reasons is the pressure for privatization of companies. Another reason is the rapid growth in the economies. The third reason is the expected large demand for new capital after the NAFTA has been approved.

American Depository Receipts (ADR)

An ADR is a receipt that has a number of foreign shares remaining on deposit with the U.S. depositorys custodian in the issuers home market. The bank is a transfer agent for the ADRs that are traded in the United States exchanges or in the OTC market.

ADRs offer various investment advantages. These advantages include −

ADRs are denominated in dollars, trade on a US stock exchange, and can be purchased through the investors regular broker. This is easier than purchasing and trading in US stocks by entering the US exchanges.

Dividends received on the shares are issued in dollars by the custodian and paid to the ADR investor, and a currency conversion is not required.

ADR trades clear in three business days as do U.S. equities, whereas settlement of underlying stocks vary in other countries.

ADR price quotes are in U.S. dollars.

ADRs are registered securities and they offer protection of ownership rights. Most other underlying stocks are bearer securities.

An ADR can be sold by trading the ADR to another investor in the US stock market, and shares can also be sold in the local stock market.

ADRs frequently represent a set of underlying shares. This allows the ADR to trade in a price range meant for US investors.

ADR owners can provide instructions to the depository bank to vote the rights.

There are two types of ADRs: sponsored and unsponsored.

Sponsored ADRs are created by a bank after a request of the foreign company. The sponsoring bank offers lots of services, including investment information and the annual report translation. Sponsored ADRs are listed on the US stock markets. New ADR issues must be sponsored.

Unsponsored ADRs are generally created on request of US investment banking firms without any direct participation of the foreign issuing firm.

Global Registered Shares (GRS)

GRS are a share that are traded globally, unlike the ADRs that are receipts of the bank deposits of home-market shares and are traded on foreign markets. The GRS are fully transferrable GRS purchased on one exchange can be sold on another. They usually trade in both US dollars and euros.

The main advantage of GRS over ADRs is that all shareholders have equal status and the direct voting rights. The main disadvantage is the cost of establishing the global registrar and the clearing facility.

Factors Affecting International Equity Returns

Macroeconomic factors, exchange rates, and industrial structures affect international equity returns.

Macroeconomic Factors

Solnik (1984) examined the effect of exchange rate fluctuations, interest rate differences, the domestic interest rate, and changes in domestic inflation expectations. He found that international monetary variables had only weak influence on equity returns. Asprem (1989) stated that fluctuations in industrial production, employment, imports, interest rates, and an inflation measure affect a small portion of the equity returns.

Exchange Rates

Adler and Simon (1986) tested the sample of foreign equity and bond index returns to exchange rate changes. They found that exchange rate changes generally had a variability of foreign bond indexes than foreign equity indexes. However, some foreign equity markets were more vulnerable to exchange rate changes than the foreign bond markets.

Industrial Structure

Roll (1992) concluded that the industrial structure of a country was important in explaining a significant part of the correlation structure of international equity index returns.

In contrast, Eun and Resnick (1984) found that the correlation structure of international security returns could be better estimated by recognized country factors rather than industry factors.

Heston and Rouwenhorst (1994) stated that industrial structure explains very little of the cross-sectional difference in country returns volatility, and that the low correlation between country indices is almost completely due to country-specific sources of variation.

Exchange Rate Forecasts

Economists and investors always tend to forecast the future exchange rates so that they can depend on the predictions to derive monetary value. There are different models that are used to find out the future exchange rate of a currency.

However, as is the case with predictions, almost all of these models are full of complexities and none of these can claim to be 100% effective in deriving the exact future exchange rate.

Exchange Rate Forecasts are derived by the computation of value of vis--vis other foreign currencies for a definite time period. There are numerous theories to predict exchange rates, but all of them have their own limitations.

Exchange Rate Forecast: Approaches

The two most commonly used methods for forecasting exchange rates are −

Fundamental Approach − This is a forecasting technique that utilizes elementary data related to a country, such as GDP, inflation rates, productivity, balance of trade, and unemployment rate. The principle is that the true worth of a currency will eventually be realized at some point of time. This approach is suitable for long-term investments.

Technical Approach − In this approach, the investor sentiment determines the changes in the exchange rate. It makes predictions by making a chart of the patterns. In addition, positioning surveys, moving-average trend-seeking trade rules, and Forex dealers customer-flow data are used in this approach.

Exchange Rate Forecast: Models

Some important exchange rate forecast models are discussed below.

Purchasing Power Parity Model

The purchasing power parity (PPP) forecasting approach is based on the Law of One Price. It states that same goods in different countries should have identical prices. For example, this law argues that a chalk in Australia will have the same price as a chalk of equal dimensions in the U.S. (considering the exchange rate and excluding transaction and shipping costs). That is, there will be no arbitrage opportunity to buy cheap in one country and sell at a profit in another.

Depending on the principle, the PPP approach predicts that the exchange rate will adjust by offsetting the price changes occurring due to inflation. For example, say the prices in the U.S. are predicted to go up by 4% over the next year and the prices in Australia are going to rise by only 2%. Then, the inflation differential between America and Australia is:

4% 2% = 2%

According to this assumption, the prices in the U.S. will rise faster in relation to prices in Australia. Therefore, the PPP approach would predict that the U.S. dollar will depreciate by about 2% to balance the prices in these two countries. So, in case the exchange rate was 90 cents U.S. per one Australian dollar, the PPP would forecast an exchange rate of −

(1 + 0.02) (US $0.90 per AUS $1) = US $0.918 per AUS $1

So, it would now take 91.8 cents U.S. to buy one Australian dollar.

Relative Economic Strength Model

The relative economic strength model determines the direction of exchange rates by taking into consideration the strength of economic growth in different countries. The idea behind this approach is that a strong economic growth will attract more investments from foreign investors. To purchase these investments in a particular country, the investor will buy the country's currency increasing the demand and price (appreciation) of the currency of that particular country.

Another factor bringing investors to a country is its interest rates. High interest rates will attract more investors, and the demand for that currency will increase, which would let the currency to appreciate.

Conversely, low interest rates will do the opposite and investors will shy away from investment in a particular country. The investors may even borrow that country's low-priced currency to fund other investments. This was the case when the Japanese yen interest rates were extremely low. This is commonly called carry-trade strategy.

The relative economic strength approach does not exactly forecast the future exchange rate like the PPP approach. It just tells whether a currency is going to appreciate or depreciate.

Econometric Models

It is a method that is used to forecast exchange rates by gathering all relevant factors that may affect a certain currency. It connects all these factors to forecast the exchange rate. The factors are normally from economic theory, but any variable can be added to it if required.

For example, say, a forecaster for a Canadian company has researched factors he thinks would affect the USD/CAD exchange rate. From his research and analysis, he found that the most influential factors are: the interest rate differential (INT), the GDP growth rate differences (GDP), and the income growth rate (IGR) differences.

The econometric model he comes up with is −

USD/CAD (1 year) = z + a(INT) + b(GDP) + c(IGR)

Now, using this model, the variables mentioned, i.e., INT, GDP, and IGR can be used to generate a forecast. The coefficients used (a, b, and c) will affect the exchange rate and will determine its direction (positive or negative).

Time Series Model

The time series model is completely technical and does not include any economic theory. The popular time series approach is known as the autoregressive moving average (ARMA) process.

The rationale is that the past behavior and price patterns can affect the future price behavior and patterns. The data used in this approach is just the time series of data to use the selected parameters to create a workable model.

To conclude, forecasting the exchange rate is an ardent task and that is why many companies and investors just tend to hedge the currency risk. Still, some people believe in forecasting exchange rates and try to find the factors that affect currency-rate movements. For them, the approaches mentioned above are a good point to start with.

Exchange Rate Fluctuations

Exchange rate fluctuations affect not only multinationals and large corporations, but also small and medium-sized enterprises. Therefore, understanding and managing exchange rate risk is an important subject for business owners and investors.

There are various kinds of exposure and related techniques for measuring the exposure. Of all the exposures, economic exposure is the most important one and it can be calculated statistically.

Companies resort to various strategies to contain economic exposure.

Types of Exposure

Companies are exposed to three types of risk caused by currency volatility −

Transaction exposure − Exchange rate fluctuations have an effect on a companys obligations to make or receive payments denominated in foreign currency in future. Transaction exposure arises from this effect and it is short-term to medium-term in nature.

Translation exposure − Currency fluctuations have an effect on a companys consolidated financial statements, particularly when it has foreign subsidiaries. Translation exposure arises due to this effect. It is medium-term to long-term in nature.

Economic (or operating) exposure − Economic exposure arises due to the effect of unpredicted currency rate fluctuations on the companys future cash flows and market value. Unanticipated exchange rate fluctuations can have a huge effect on a companys competitive position.

Note that economic exposure is impossible to predict, while transaction and translation exposure can be estimated.

Economic Exposure An Example

Consider a big U.S. multinational with operations in numerous countries around the world. The companys biggest export markets are Europe and Japan, which together offer 40% of the companys annual revenues.

The companys management had factored in an average slump of 3% for the dollar against the Euro and Japanese Yen for the running and the next two years. The management expected that the Dollar will be bearish due to the recurring U.S. budget deadlock, and growing fiscal and current account deficits, which they expected would affect the exchange rate.

However, the rapidly improving U.S. economy has triggered speculation that the Fed will tighten monetary policy very soon. The Dollar is rallying, and in the last few months, it has gained about 5% against the Euro and the Yen. The outlook suggests further gains, as the monetary policy in Japan is stimulative and the European economy is coming out of recession.

The U.S. company is now facing not just transaction exposure (as its large export sales) and translation exposure (as it has subsidiaries worldwide), but also economic exposure. The Dollar was expected to decline about 3% annually against the Euro and the Yen, but it has already gained 5% versus these currencies, which is a variance of 8 percentage points at hand. This will have a negative effect on sales and cash flows. The investors have already taken into account the currency fluctuations and the stock of the company fell 7%.

Calculating Economic Exposure

Foreign asset or overseas cash flow value fluctuates with the exchange rate changes. We know from statistics that a regression analysis of the asset value (P) versus the spot exchange rate (S) will offer the following regression equation −

P = a + (b x S) + e

Where, a is the regression constant, b is the regression coefficient, and e is a random error term with a mean of zero. Here, b is a measure of economic exposure, and it measures the sensitivity of an assets dollar value to the exchange rate.

The regression coefficient is the ratio of the covariance between the asset value and the exchange rate, to the variance of the spot rate. It is expressed as −

Economic Exposure Numerical Example

A U.S. company (let us call it USX) has a 10% stake in a European company say EuroStar. USX is concerned about a decline in the Euro, and as it wants to maximize the Dollar value of EuroStar. It would like to estimate its economic exposure.

USX thinks the probabilities of a stronger and/or weaker Euro is equal, i.e., 5050. In the strong-Euro scenario, the Euro will be at 1.50 against the Dollar, which would have a negative impact on EuroStar (due to export loss). Then, EuroStar will have a market value of EUR 800 million, valuing USXs 10% stake at EUR 80 million (or $120 million).

In the weak-Euro scenario, currency will be at 1.25; EuroStar would have a market value of EUR 1.2 billion, valuing USXs 10% stake will be equal to $150 million.

If P represents the value of USXs 10% stake in EuroStar in Dollar terms, and S represents the Euro spot rate, then the covariance of P and S is −

Cov (P,S) = 1.875

Var (S) = 0.015625

Therefore, b = 1.875 ÷ (0.015625) = EUR 120 million

USXs economic exposure is a negative EUR 120 million, which is equivalent to saying that the value of its stake in EuroStar decreases as the Euro gets stronger, and increases as the Euro weakens.

Determining Economic Exposure

The economic exposure is usually determined by two factors −

Whether the markets where the company inputs and sells its products are competitive or monopolistic? Economic exposure is more when either a firms input costs or goods prices are related to currency fluctuations. If both costs and prices are relative or secluded to currency fluctuations, the effects are cancelled by each other and it reduces the economic exposure.

Whether a firm can adjust to markets, its product mix, and the source of inputs in a reply to currency fluctuations? Flexibility would mean lesser operating exposure, while sternness would mean a greater operating exposure.

Managing Economic Exposure

The economic exposure risks can be removed through operational strategies or currency risk mitigation strategies.

Operational strategies

Diversifying production facilities and markets for products − Diversification mitigates the risk related with production facilities or sales being concentrated in one or two markets. However, the drawback is the company may lose economies of scale.

Sourcing flexibility − Having sourcing flexibilities for key inputs makes strategic sense, as exchange rate moves may make inputs too expensive from one region.

Diversifying financing − Having different capital markets gives a company the flexibility to raise capital in the market with the cheapest cost.

Currency risk mitigation strategies

The most common strategies are −

Matching currency flows − Here, foreign currency inflows and outflows are matched. For example, if a U.S. company having inflows in Euros is looking to raise debt, it must borrow in Euros.

Currency risk-sharing agreements − It is a sales or purchase contract of two parties where they agree to share the currency fluctuation risk. Price adjustment is made in this, so that the base price of the transaction is adjusted.

Back-to-back loans − Also called as credit swap, in this arrangement, two companies of two nations borrow each others currency for a defined period. The back-to-back loan stays as both an asset and a liability on their balance sheets.

Currency swaps − It is similar to a back-to-back loan, but it does not appear on the balance sheet. Here, two firms borrow in the markets and currencies so that each can have the best rates, and then they swap the proceeds.

Foreign Currency Futures & Options

Depending on the selection of buying or selling the numerator or denominator of a currency pair, the derivative contracts are known as futures and options.

There are various ways to earn a profit from futures and options, but the contract-holder is always obliged to certain rules when they go into a contract.

There are some basic differences between futures and options and these differences are the ways through which investors can make a profit or a loss.

Long and Short Currency Trading

Currency futures and options are derivative contracts. These contracts derive their own values from utilization of the underlying assets, which, in this case, are currency pairs. Currencies are always traded in pairs.

For example, the Euro and U.S. Dollar pair is expressed as EUR/USD. When someone buys this pair, they are said to be going long (buying) with the numerator, or the base, currency, which is the Euro; and thereby selling the denominator (quote) currency, which is the Dollar. When someone sells the pair, it is selling the Euro and buying the Dollar. When the long currency appreciates against the short currency, people make money.

Foreign Currency Futures

Currency futures make the buyer of the contract to buy the long currency (numerator) by paying with the short currency (denominator) for it. The seller of a contract has the reverse obligation. The obligation of the contact is usually due on the expiration date of the future.

The ratio of currencies, bought and sold, is settled in advance between the parties involved. People make a profit or loss depending on the gap between the settled price and the real, effective price on the date of expiration.

Margins are deposited for the futures trades cash is the important part that serves as the performance bond to make sure that both parties are obliged to fulfil their obligations.

Options on Currency Pairs

The party that purchases a currency pair call option may also decide to settle for an execution or to sell out the option on or before the date of expiration. There is a strike price of the option that shows a particular exchange ratio for the given pair of currencies.

When the actual price of the currency pair is more than the strike price, the call holder earns a profit. It is said to execute the option by buying the base and selling the quote at a profitable term. A put buyer always bets on the denominator or quote currency appreciating against the numerator or the base currency.

Options on Currency Futures