- Managerial Economics - Home

- Managerial Economics Overview

- Business Firms & Decisions

- Economic Analysis & Optimizations

- Regression Technique

- Production & Cost Analysis

- Theory of Production

- Cost & Breakeven Analysis

- Market Structure & Pricing Theory

- Market Structure & Pricing Decisions

- Pricing Strategies

- Capital Budgeting

- Investment Under Certainty

- Investment Under Uncertainty

- Macroeconomic Aspects

- Macroeconomics Basics

- Circular Flow Model of Economy

- National Income & Measurement

- National Income Determination

- Theories of Economic Growth

- Business Cycles & Stabilization

- Inflation & ITS Control Measures

- Managerial Economics Resources

- Managerial Economics - Quick Guide

- Managerial Economics - Resources

- Managerial Economics - Discussion

Market System & Equilibrium

In economics, a market refers to the collective activity of buyers and sellers for a particular product or service.

The Economic Systems

Economic market system is a set of institutions for allocating resources and making choices to satisfy human wants. In a market system, the forces and interaction of supply and demand for each commodity determines what and how much to produce.

In price system, the combination is based on least combination method. This method maximizes the profit and reduces the cost. Thus firms using least combination method can lower the cost and make profit. Resources are allocated by planning. In a market economy, goods are allocated according to the decisions of producers and consumers.

Pure Capitalism − Pure capitalism market economic system is a system in which individuals own productive resources and as it is the private ownership; they can be used in any manner subject to the productive legal restrictions.

Communism − Communism is an economy in which workers are motivated to contribute to the economy. Government has most of the control in this system. The government decides what to produce, how much, and how to produce. This is an economic decision making through planned economy.

Mixed Economy − Mixed economy is a system where most of the wealth is generated by businesses and the government also plays an important role.

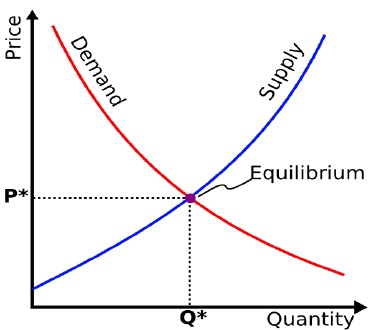

Demand and Supply Curves

The market demand curve indicates the maximum price that buyers will pay to purchase a given quantity of the market product.

The market supply curve indicates the minimum price that suppliers would accept to be willing to provide a given supply of the market product.

In order to have buyers and sellers agree on the quantity that would be provided and purchased, the price needs to be a right level. The market equilibrium is the quantity and associated price at which there is concurrence between sellers and buyers.

Now lets have a look at the typical supply and demand curve presentation.

From the above graphical presentation, we can clearly see the point at which the supply and demand curves intersect with each other which we call as Equilibrium point.

Market Equilibrium

Market equilibrium is determined at the intersection of the market demand and market supply. The price that equates the quantity demanded with the quantity supplied is the equilibrium price and amount that people are willing to buy and sellers are willing to offer at the equilibrium price level is the equilibrium quantity.

A market situation in which the quantity demanded exceeds the quantity supplied shows the shortage of the market. A shortage occurs at a price below the equilibrium level. A market situation in which the quantity supplied exceeds the quantity demanded, there exists the surplus of the market. A surplus occurs at a price above the equilibrium level.

If a market is not at equilibrium, market forces try to move it equilibrium. Lets have a look − If the market price is above the equilibrium value, there is an excess of supply in the market, which means there is more supply than demand. In this situation, sellers try to reduce the price of their good to clear their inventories. They also slow down their production. The lower price helps more people to buy, which reduces the supply further. This process further results in increase in demand and decrease in supply until the market price equals the equilibrium price.

If the market price is below the equilibrium value, then there is excess in demand. In this case, buyers bid up the price of the goods. As the price goes up, some buyers tend to quit trying because they don't want to, or can't pay the higher price. Eventually, the upward pressure on price and supply will stabilize at market equilibrium.