Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

What is net investment hedge?

It is a specific type of foreign currency cash flow hedge used to reduce or eliminate risk arises to foreign currency of an entity’s net investment in a foreign operation. In other words, it is the hedge designed to remove entity’s changes in net investment value to foreign investment in a foreign operation. That foreign operation occurs due to change in foreign exchange rates between local currency of foreign investee and reporting currency of investor.

The hedging instrument in his hedge can be derivative, non-derivatives or a combination of both. Derivatives like foreign exchange forward contract and non-derivative like foreign currency denominated debt instruments.

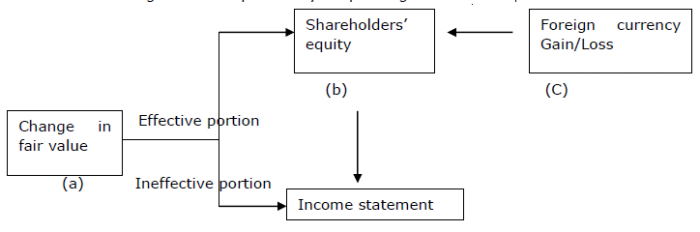

Derivative financial instruments are considered as net investment hedge as a part of cumulative transaction agreement, effective proportions of profit or loss (hedging instrument) are entered in accumulated comprehensive income and ineffective portions are entered in other expenses during period of change.

If derivative hedging instrument is used, then

- Effective change in fair value is identified in equity.

- Ineffective portion is identified in profit or loss.

If non-derivative instrument is used, then gain or loss in foreign currency translation is identified in equity.

Net investment hedge can be explained by simple diagram as follows

Here

a) Measurement of derivative, b) Recognition and c) net investment in foreign operation.

Net investment hedge in foreign operations

Overseas equity investment (subsidiary, joint venture or associate) is hedged by derivative or non-derivative contract. It comes under IAS21

Other comprehensive income (OCI) − effective portion of foreign currency Gain/loss on hedging instrument

Profit/loss − ineffective portion

When disposed of cumulative Gains/Loss in OCI shall be recognized as part of Profit/Loss (on disposal)

2K+ Views