Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

What is an asset deal in merger and acquisition?

If the buyer wants to purchase an operating asset instead of shares in a merger and acquisition transaction, then that deal is called an asset deal. An asset deal is not a form of acquisition. It comes under transfer of business units/assets.

To complete the asset deal transaction, an asset purchase agreement is made between the buyer and the seller. This agreement outlines the asset purchased.

Asset purchase agreement (APA) includes payment structure, representations, considerations, warranties, legal structures etc.

Asset purchase agreement

Asset purchase agreement is used to complete the asset deal transaction. The agreement outlines the specific assets (which will be purchased), total considerations, warranties, terms and conditions, legal terms etc.

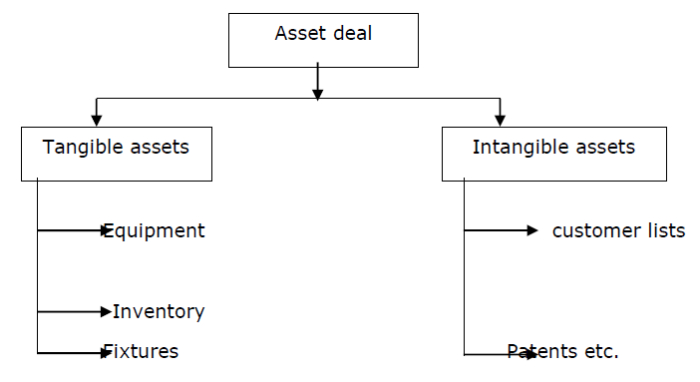

Asset purchased can be a tangible asset or intangible asset. Equipment, fixtures and inventory comes under tangible assets. Patents, customer list etc. come under intangible assets.

In the balance sheet, Sellers record the sale, their long term assets will go down, cash goes as transaction proceeds, gain or loss is recorded in the income statement. Buyer will record the investment in the asset account.

Types

The types of an asset deal are as follows −

Benefits

The benefits of an asset deal are as follows −

Assets can be selected by the buyer.

It provides tax benefits.

Liabilities (stock exchange) can be avoided.

Gives buyers the ability to divest.

Disadvantages

The disadvantages of an asset deal are as follows −

Takes longer time.

Needs longer preparations.

More negotiations.

Example

Company 1 buys all assets of company 2 which includes intangible assets and IP and total liabilities of $27.2 billion (let us assume). Now company 2 gets $27.2 billion (not its shareholders).

After getting the amount, now the company issues a dividend of $196 per share to its shareholders and no taxes are paid on sale gain at corporate level. Shares are not cancelled after getting dividends, now they have shares in a company with no assets and liabilities. Shares are now worth less and the company can be liquidated.

417 Views