Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

What is Amortization?

Amortization vs. Depreciation

Both Amortization and Depreciation are concepts that are used to account for the consumption of assets and how they lose their value over their useful life.

We understand that tangible assets such as plant machinery, furniture, buildings, and vehicles lose their value over a period, which is called "depreciation". But, what about intangible assets such as copyrights, trademarks, patents, agreements, etc.? Such intangible assets too lose their value over a course of their useful economic life.

Amortization is a concept similar to depreciation, but it is applied primarily to intangible assets and their periodic reduction in value over time. The rules of amortization are different for −

Amortization of assets, and

Amortization of loans.

Amortization of Assets

Amortization is the process of factoring in the cost of an intangible asset over the course of its useful life. Amortization accounts for the consumption of intangible assets over its lifetime.

Amortization can be contributed to reducing the book value of a company's intangible assets, by gradually lowering their value.

Amortization is recorded as an expense in the financial statements, hence it can be utilized to reduce the taxable income of a company.

Amortization of assets is difficult to calculate because we don't have a fixed parameter to recognize the true value of an intangible asset like a patent.

Amortization of Loans

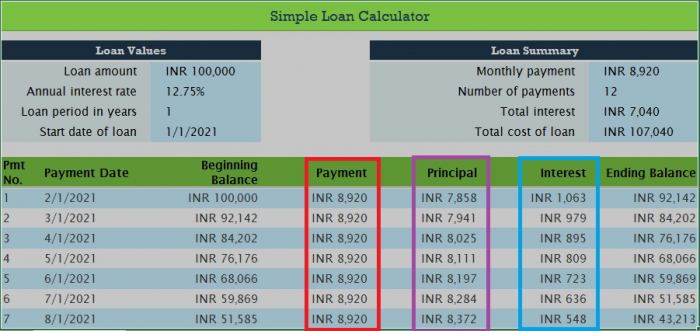

Amortization of loans is a mechanism which breaks the loan amount into equal fixed installments, with each installment having an increasing "principal" component and a gradually reducing "interest" component. It uses an amortization schedule to make sure a greater portion of the loan repayment goes towards the "interest" component in the early stages of the loan.

In the following example, observe how the installment amount remains fixed throughout the tenure, but the principal and interest amounts paid on the loan varies from one month to the next. The Interest component is maximum in the early stages of repayment.

Amortized loans are popular among the lenders as well as the debtors because there is a fixed tenure within which the entire loan has to be paid off. It ensures that the lender receives the repayments in a timely manner and the debtor is not overburdened with debt.

Regardless of whether it is an Amortized asset or an Amortized loan, it always refers to the periodic lowering of the book value in a predefined period of time.

No Salvage Value in Amortization

In depreciation, when the cost of a tangible asset is completely written off, there still remains a resale value at the end which is known as the "salvage value." It is this salvage value that is deducted from the original cost at the time of calculating the depreciation costs.

In contrast, Amortized assets or loans don't have any salvage value because they are not physical or tangible assets.

In amortization, the reduction in value is always calculated in a straightline method. It means the same amount is expensed every year. This is in contrast to depreciation where we can have tangible assets like vehicles which are eligible for accelerated depreciation.

332 Views