Data Structure

Data Structure Networking

Networking RDBMS

RDBMS Operating System

Operating System Java

Java MS Excel

MS Excel iOS

iOS HTML

HTML CSS

CSS Android

Android Python

Python C Programming

C Programming C++

C++ C#

C# MongoDB

MongoDB MySQL

MySQL Javascript

Javascript PHP

PHP

- Selected Reading

- UPSC IAS Exams Notes

- Developer's Best Practices

- Questions and Answers

- Effective Resume Writing

- HR Interview Questions

- Computer Glossary

- Who is Who

Marginal Cost Formula

What is Marginal Cost?

Mostly used in the manufacturing industry, marginal cost refers to the extra cost required to produce additional items. The marginal cost is calculated by dividing additional costs by the change in quantity. The calculation also includes the items that have already been produced and variable costs that must be accounted for the additional items.

Marginal cost is the change of cost with a change in the level of production. When marginal costs are below the price per unit of a good, the manufacturer may earn a profit from the item.

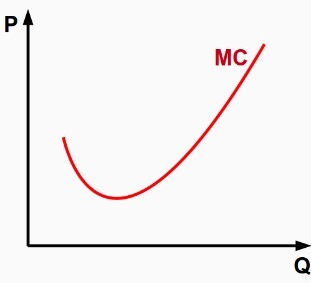

Plotting marginal cost on a graph shows a U-shaped pattern where the costs start high but go down as the production goes up. After a certain point, the costs rise again. In many cases, the marginal cost of production decreases with increasing production. This happens because the price per unit goes down as the number of items produced goes up. Alternatively, the marginal cost of an item may go up with decreasing production of that item.

Marginal Cost Formula: Calculation

In order to calculate marginal costs, one must first find out the change in costs and the change in production quantity.

-

Change in costs Costs can fluctuate depending on the output volume of the products manufactured.

For example, if two more employees are required to produce the same amount of goods, then an increase in the costs would occur. The change in costs is calculated by subtracting the production costs in the first output run from the cost of the next output run.

-

Change in production quantity The quantity of production may change depending on demand and therefore increase and decrease in production may take place.

For example, if a company produces 5,000 pairs of shoes but needs to produce 10,000 more, the change in production quantity can be found by subtracting the initial output from the final or next output of the production volume.

Marginal cost can be calculated with the following formula

$\mathrm{Marginal\:Cost\:=\:Change\:in\:costs\:/\:Change\:in\:quantity}$

Example

Suppose

Current number of units of pens produced by a company = 5,000 units

Future number of units of pens produced by a company = 6,000 units

The current cost of production = Rs 25,000

The future cost of production = Rs 30,000

$$\mathrm{Marginal\:cost\:=\:\frac{30,000?25,000}{6,000?5000}}$$

Marginal Cost = Rs 5

Benefits of Marginal Cost

Marginal cost is an important part of financial analysis. There is a host of benefits that can be obtained from the calculation of marginal costs.Some of these benefits include the following

Marginal cost shows the areas where the excess marginal revenue is at its highest against the marginal cost. Understanding these areas help businesses learn about costly scenarios or points where the businesses must concentrate their focus to bring costs down.

Marginal cost also shows the increased or decreased costs of production. This shows the companies how much they pay for producing additional items. This in turn helps the businesses evaluate the profitability of an item before it is taken to the market.

Marginal cost also helps the companies determine the cost advantage and shows when the company can optimize the operations to gain maximum output along with maximum profits from each item produced.

Marginal cost also shows when the company can reduce the cost of a product keeping the revenue intact. Therefore, it shows the points where production has the largest impact.

Marginal costs also show whether companies should follow the current production patterns or increase the price of the items to continue having profitability over the produced items.

Marginal cost calculation also shows whether the prices of items must be increased to offset any potential loss.

Key Takeaways

The marginal cost of a company refers to the extra amount of cost required to produce additional units of goods and services. This is important because companies need to have an eye on additional expenses required to meet the increasing or decreasing output of a product.

Realizing the changes in costs and quantities are important measures in the calculation of marginal cost. For example, production costs may increase depending on whether the output is decreased or increased. The change in production volume is dependent on inventory measures at various points of the production output position.

Marginal cost offers a host of benefits. For example, companies can increase their production efficiency and decide whether to increase the prices in order to fend off any potential loss.

The formula for Marginal cost = Change in cost/Change in quantity.

Examples of Marginal Cost usability

Example 1

Sunrise industries manufacture seat covers for cars and it produces 300,000 units of covers for a production cost of Rs 4,800,000. However, the demand in the market has now increased for which the company needs to hire more employees and increase the production volume. The number of units required for the next production cycle is 320,000 units for which the cost of production is Rs 5,200,000. So, the marginal cost for the company:

$$\mathrm{\frac{Change\:in\:cost}{Change\:in\:quantity}}$$

$$\mathrm{\frac{5,200,000\:?\:4,800,000}{320,000\:?\:300,000}}$$

$$\mathrm{\frac{400}{20}}$$

$$\mathrm{=\:\:Rs\:20\:is\:the\:marginal\:cost}$$

Example 2

Let's assume that a company makes pencil. Each pencil requires a lead costing Rs 2. The costs of lead are variable. The pencil factory has an expense of Rs 150,000 in fixed costs per month.

If the company makes 15,000 pencil per month then the company incurs Rs 10 of fixed

$\mathrm{\lgroup\frac{150,000}{15,000}\rgroup}$

The total cost of the pencil would be Rs 12 (Rs 10 fixed + Rs 2 for lead).

Now if the pen maker wants to increase the production volume to 20,000 pens per month then the cost for each pen would be fixed at $\mathrm{\lgroup\frac{150,000}{15,000}\rgroup\:=\:Rs\:7.5\:per\:pencil.}$

Now, the total cost for each pen would decrease to Rs 7.5 + 2 = Rs 9.5 per pen . Here, an increased production volume has decreased the price of the product.

Conclusion

Understanding marginal cost is important for companies because it shows whether the price of an item should be increased to avoid future losses arising out of the production in future. Therefore, it is a very important tool for business organizations. Good use of marginal cost can save companies from incurring losses and hence it has widespread uses in the manufacturing industries.

FAQs

Qns 1. What is marginal cost? How is it calculated?

Ans. Marginal cost refers to the extra cost required to produce additional items. The marginal cost is calculated by dividing additional costs by the change in quantity. The calculation also includes the items that have already been produced and variable costs that must be accounted for the additional items.

Qns 2. What is the marginal cost formula?

Ans. Marginal cost is calculated with the following formula:

Qns 3. Give one benefit of using marginal cost.

Ans. Marginal cost offers a host of benefits. For example, companies can increase their production efficiency and decide whether to increase the prices in order to fend off any potential loss.

280 Views