- Financial Accounting - Home

- Rectification of Errors

- Capital and Revenue

- Final Accounts

- Provision and Reserves

- Measurement of Business Income

- Bills of Exchange & Promissory Notes

- Inventory Valuation

- Analysis of Changes in Income

- Accounting for Consignment

- Joint Venture

- Non-Trading Accounts

- Single Entry

- Leasing

- Investment Account

- Insolvency Accounts

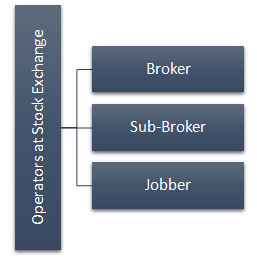

- Stock Exchange Transactions

- Accounts of Private Individuals

- Co-Operative Societies

- Insurance Claims

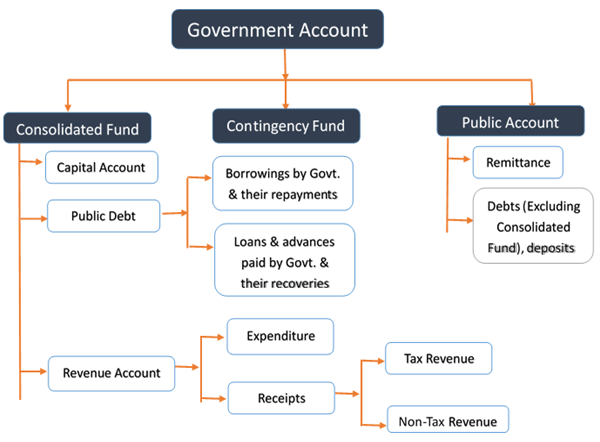

- Government Accounting

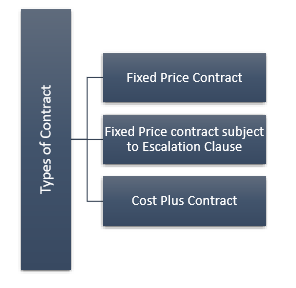

- Contract Account

- Departmental Accounting

- Voyage Accounting

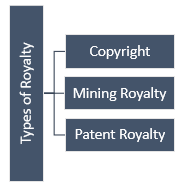

- Royalty Accounts

- Financial Accounting - Quick Guide

- Financial Accounting - Resources

- Financial Accounting - Discussion

Financial Accounting - Quick Guide

Financial Accounting - Rectification of Errors

Financial accounting deals with recording and maintaining every monetary transaction of an organization. However, sometimes, a few entries might be either incorrect or used at the wrong place. In financial accounting, the process of correcting such mistakes is known as Rectification of Errors.

Types of Errors

Two most common types of errors, which are usually occurred at the time of preparation of Financial Statements are discussed below.

Error which Effect only One Account

- Omission of posting of balance in a Trial Balance.

- Error of carried forward of balance.

- Error of casting and posting.

Error which Effect Two or more Accounts

The nature of errors, which occur during the preparation of Financial Statements are −

- Error of posting in wrong account.

- Error of principle.

- Error of omission.

Methods of Rectification of Errors

There are three types of methods used in rectification of Errors −

Replacing Correct Figure by Striking Off the Wrong Figure

For example, cash payment of Rs. 989 on the account of stationery purchased written as Rs. 998, will be corrected as −

Cash Book

By Stationery A/c |

989 |

Through Journal Entry

Normally, there are three types of errors, which can be rectified by passing Journal Entries −

Short credited or debit in one account and excess debit or credit in another account. For example, purchase of stationery for Rs. 989 wrongly debited to purchase of raw material account will be corrected as follows −

Journal Entry

Stationery AccountDr. To Purchase Account (Being Cash purchase of stationery wrongly debited to Purchase account, now rectified) |

989 |

989 |

If, by mistake one account is debited as well as credited with wrong amount simultaneously. For example, Cash purchase of stationery of Rs. 989 booked with an amount of Rs. 489 will be corrected as follows −

Journal Entry

Stationery AccountDr. To Purchase Account (Being purchase of stationery for Rs. 989 wrongly written as Rs. 489 now rectified) |

500 |

500 |

If there is an omission of recording a transaction, it can be rectified by passing journal entry to book that omitted transaction. For example, omission of recording transaction of purchase of raw material for Rs. 5000 from Mr. X will be recorded and corrected by passing the following journal Entry −

Journal Entry

Stationery AccountDr. To X Account (Being omitted entry of purchase of Rs. 5000 from Mr. X now recorded and rectified) |

5000 |

5000 |

If there is a Mistake that Effects Trial Balance

Before closing the books and transferring the difference in suspense account and

After the agreed difference is transferred into the suspense account, following accounting treatment will be done −

Earlier entry debited or credited with fewer amount will be rectified by repeating that entry with difference amount to complete that amount. For example, entry done with Rs. 500 instead of Rs. 5000 will be rectified by doing same entry with an amount of Rs. 4500. In case, where entry wrongly debited or credited to other account may be rectified by doing reversal of old entry to nullify earlier effect.

If expense booked with less amount entry then −

Particular Expense Account To Cash/Personal Account (Being wrong amount of posting, rectified with Difference amount Rs. 4,500 (5000-500) |

Dr |

4,500 4,500 |

If income is booked with less amount, it will be rectified as −

Cash/Personal account To Income Account (Being wrong amount of posting now Rectified. 4500 (5000-500) |

Dr |

4,500 4,500 |

If posting done in wrong account that will be rectified as follows −

Stationery AccountDr.** To Office Expenses Account** (Being wrongly debited earlier in office account, now Rectified and posted in stationery account) |

In case (ii) where difference has already been transferred to suspense account, further amount will be debited or credited to respective account and correspondingly suspense account will be debited or credited. Thus, these entries would reduce/nil the balance of suspense account.

Effect of Errors on Agreement of Trial Balance

The errors by which there is no change on both side of trial balance or wrong effect on trial balance with same amount will not lead to effect on agreement of Trial Balance. Errors of omission, error of posting with wrong amount on both side, or Error of principles are the example of such errors. To find out such errors is a challenging job for any book keeper or an accountant.

Effects of Errors on Financial Statements

Effect of error depends on the nature of effected accounts. If errors relate to nominal account, it will either increase or reduce the profit and rectification will reduce excess profit or Loss. Effect of error on Trading and Profit account ultimately effect the Balance-Sheet of a company too, because reduced profit or excess profit ultimately transferred to capital account, which is a part of the Balance Sheet.

There are some errors, which effect Trading or Profit and Loss account and Balance sheet simultaneously, like entry of depreciation will affect profit as well as value of the Fixed Assets.

Some entry may effect on Balance sheet only like, for instance omission of entry of cash paid to purchase fixed assets will affect Balance Sheet of a firm only.

Rectification of Errors after Preparation of Final Accounts

To remain unaffected Profit or Loss of the current financial year, the errors, which took place in last financial years are adjusted and rotated through a Profit & Loss adjustment account. Balance of this account directly transferred to capital account of firm without affecting the current year profit or loss.

Financial Accounting - Capital and Revenue

One of the major aspects of preparing a correct financial statement is to distinguish revenue and capital in regard to revenue income, revenue expenditure, revenue payments, revenue profits, and revenue losses of the company with capital income, capital receipts, capital profit, or capital losses.

In fact, without differentiating, we cannot think of correctness of a financial statement. Ultimately, it will mislead the end results where no one can conclude anything. As per this principle, a revenue item should be recorded in the Trading and Profit & Loss account and a capital item should be recorded in the Balance-Sheet of respective firm.

Capital Expenditure

Capital expenditure is the expenditure incurred to acquire fixed assets, capital leases, office equipment, computer equipment, software development, purchase of tangible and intangible assets, and such kind of any value addition in business with the purpose to enhance the income. However, to decide nature of the capital expenditure, we need to pay attention on −

The expenditure, which benefit cannot be consumed or utilized in the same accounting period, should be treated as capital expenditure.

Expenditure incurred to acquire Fixed Assets for the company.

Expenditure incurred to acquire fixed assets, erection and installation charges, transportation of assets charges, and travelling expenses directly relates to the purchase fixed assets, are covered under capital expenditure.

Capital addition to any fixed assets, which increases the life or efficiency of those assets for example, an addition to building.

Revenue Expenditure

Revenue expenditure is the expenditure incurred on the fixed assets for the maintenance instead of increasing the earning capacity of the assets. Examples of some of the important revenue expenditures are as follows −

Wages/Salary

Freight inward & outward

Administrative Expenditure

Selling and distribution Expenditure

Assets purchased for resale purpose

Repairs and renewal expenditure which are necessary to keep Fixed Assets in good running and efficient conditions

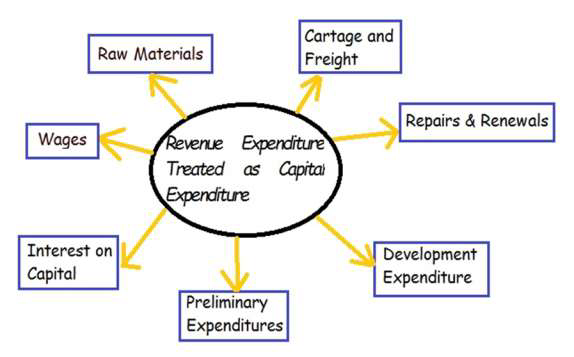

Revenue Expenditure Treated as Capital Expenditure

Following are the list of important revenue expenditures, but under certain circumstances, they are treated as a capital expenditure −

Raw Material and Consumables − If those are used in making any fixed assets.

Cartage and Freight − If those are incurred to bring Fixed Assets.

Repairs & Renewals − If incurred to enhance life of the assets or efficiency of the assets.

Preliminary Expenditures − Expenditure incurred during the formation of a business should be treated as capital expenditure.

Interest on Capital − If paid for the construction work before the commencement of production or business.

Development Expenditure − In some businesses, long period of development and heavy amount of investment are required before starting the production especially in a Tea or Rubber plantation. Usually, these expenditure should be treated as the capital expenditure.

Wages − If paid to build up assets or for the erection and installation of Plant and Machinery.

Deferred Revenue Expenditure

Some non-recurring and special nature of expenditure for which heavy amount incurred and benefit for the same will spread in up-coming years, to be treated as capital expenditure and will be shown as the assets of the firm. Part of the expenditure should be debited to Profit & Loss account every year. For example, if heavy amount paid for the advertisement of a product, which benefits are expected to be received in next four years, then it should be debited as ¼ of the part in Profit & Loss account as the revenue expenses and balance ¾ will be shown as the assets in the Balance-Sheet.

Capital and Revenue Profit

The premium received on issue of shares, and the profit on sale of fixed assets are the major examples of capital profit and should not be treated as revenue profit. Capital profit should be transferred to the capital reserve account, which is used to set off capital losses in future if any.

Capital and Revenue Receipts

Sale of fixed assets, capital employed or invested, and loans are the example of capital receipts. On the other hand, sale of stock, commission received, and interest on investment received are the main examples of revenue receipts. Revenue receipts will be credited to the profit and loss account and on the other hand, capital receipts will affect the Balance-sheet.

Capital and Revenue Losses

Discount on issue of shares and losses on sale of fixed assets are the capital loss and would be set off against the capital profits only. Revenue losses on normal business activity are part of the profit and loss account.

Financial Accounting - Final Accounts

Final Accounts are the accounts, which are prepared at the end of a fiscal year. It gives a precise idea of the financial position of the business/organization to the owners, management, or other interested parties. Financial statements are primarily recorded in a journal; then transferred to a ledger; and thereafter, the final account is prepared (as shown in the illustration).

Usually, a final account includes the following components −

- Trading Account

- Manufacturing Account

- Profit and Loss Account

- Balance Sheet

Now, let us discuss each of them in detail −

Trading Account

Trading accounts represents the Gross Profit/Gross Loss of the concern out of sale and purchase for the particular accounting period.

Study of Debit side of Trading Account

Opening Stock − Unsold closing stock of the last financial year is appeared in debit side of the Trading Account as To Opening Stock of the current financial year.

Purchases − Total purchases (net of purchase return) including cash purchase and credit purchase of traded goods during the current financial year appeared as To Purchases in the debit side of Trading Account.

Direct Expenses − Expenses incurred to bring traded goods at business premises/warehouse called direct expenses. Freight charges, cartage or carriage charges, custom and import duty in case of import, gas, electricity fuel, water, packing material, wages, and any other expenses incurred in this regards comes under the debit side of Trading Account and appeared as To Particular Name of the Expenses.

Sales Account − Total Sale of the traded goods including cash and credit sales will appear at outer column of the credit side of Trading Account as By Sales. Sales should be on net releasable value excluding Central Sales Tax, Vat, Custom, and Excise Duty.

Closing Stock − Total Value of unsold stock of the current financial year is called as closing stock and will appear at the credit side of Trading Account.

closing Stock = Opening Stock + Net Purchases - Net Sale

Gross Profit − Gross profit is the difference of revenue and the cost of providing services or making products. However, it is calculated before deducting payroll, taxation, overhead, and other interest payments. Gross Margin is used in the US English and carries same meaning as the Gross Profit.

Gross Profit = Sales - Cost of Goods Sold

Operating Profit − Operating profit is the difference of revenue and the costs generated by ordinary operations. However, it is calculated before deducting taxes, interest payments, investment gains/losses, and many other non-recurring items.

Operating Profit = Gross Profit - Total Operating Expenses

Net Profit − Net profit is the difference of total revenue and the total expenses of the company. It is also known as net income or net earnings.

Net Profit = Operating Profit - (Taxes + Interest)

Format of Trading Account

|

Trading Account of M/s ABC Limited (For the period ending 31-03-2014) |

|||

| Particulars | Amount | Particulars | Amount |

| To Opening Stock | XX | By Sales | XX |

| To Purchases | XX | By Closing Stock | XX |

| To Direct Expenses | XX | By Gross Loss c/d | XXX |

| To Gross Profit c/d | XXX | ||

| Total | XXXX | Total | XXXX |

Manufacturing Account

Manufacturing account prepared in a case where goods are manufactured by the firm itself. Manufacturing accounts represent cost of production. Cost of production then transferred to Trading account where other traded goods also treated in a same manner as Trading account.

Important Point Related to Manufacturing Account

Apart from the points discussed under the section of Trading account, there are a few additional important points that need to be discuss here −

Raw Material − Raw material is used to produce products and there may be opening stock, purchases, and closing stock of Raw material. Raw material is the main and basic material to produce items.

Work-in-Progress − Work-in-progress means the products, which are still partially finished, but they are important parts of the opening and closing stock. To know the correct value of the cost of production, it is necessary to calculate the correct cost of it.

Finished Product − Finished product is the final product, which is manufactured by the concerned business and transferred to trading account for sale.

Raw Material Consumed (RMC) − It is calculated as.

Cost of Production − Cost of production is the balancing figure of Manufacturing account as per the format given below.

RMC = Opening Stock of Raw Material + Purchases - Closing Stock

|

Manufacturing Account (For the year ending.) |

|||

| Particulars | Amount | Particulars | Amount |

| To Opening Stock of Work-in-Progress | XX | By Closing Stock of Work-in-Progress | XX |

| To Raw Material Consumed | XX | By Scrap Sale | XX |

| To Wages | XXX | By Cost of Production | XXX |

| To Factory overheadxx | (Balancing figure) | ||

| Power or fuelxx | |||

| Dep. Of Plantxx | |||

| Rent- Factoryxx | Other Factory Exp.xx | xxx | |

| Total | XXXX | Total | XXXX |

Profit and Loss Account

Profit & Loss account represents the Gross profit as transferred from Trading Account on the credit side of it along with any other income received by the firm like interest, Commission, etc.

Debit side of profit and loss account is a summary of all the indirect expenses as incurred by the firm during that particular accounting year. For example, Administrative Expenses, Personal Expenses, Financial Expenses, Selling, and Distribution Expenses, Depreciation, Bad Debts, Interest, Discount, etc. Balancing figure of profit and loss accounts represents the true and net profit as earned at the end of the accounting period and transferred to the Balance Sheet.

|

Profit & Loss Account of M/s (For the period ending ..) |

|||

| Particulars | Amount | Particulars | Amount |

| To Salaries | XX | By Gross Profit b/d | XX |

| To Rent | XX | ||

| To Office Expenses | XX | By Bank Interest received | XX |

| To Bank charges | XX | By Discount | XX |

| To Bank Interest | XX | By Commission Income | XX |

| To Electricity Expenses | XX | By Net Loss transfer to Balance sheet | XX |

| To Staff Welfare Expenses | XX | ||

| To Audit Fees | XX | ||

| To Repair & Renewal | XX | ||

| To Commission | XX | ||

| To Sundry Expenses | XX | ||

| To Depreciation | XX | ||

| To Net Profit transfer to Balance sheet | XX | ||

| Total | XXXX | Total | XXXX |

Balance Sheet

A balance sheet reflects the financial position of a business for the specific period of time. The balance sheet is prepared by tabulating the assets (fixed assets + current assets) and the liabilities (long term liability + current liability) on a specific date.

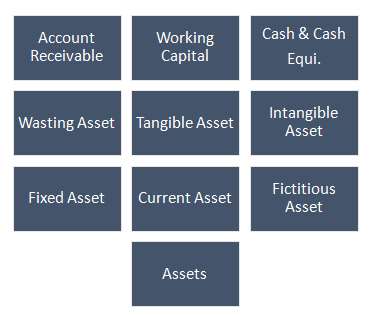

Assets

Assets are the economic resources for the businesses. It can be categorized as −

Fixed Assets − Fixed assets are the purchased/constructed assets, used to earn profit not only in current year, but also in next coming years. However, it also depends upon the life and utility of the assets. Fixed assets may be tangible or intangible. Plant & machinery, land & building, furniture, and fixture are the examples of a few Fixed Assets.

Current Assets − The assets, which are easily available to discharge current liabilities of the firm called as Current Assets. Cash at bank, stock, and sundry debtors are the examples of current assets.

Fictitious Assets − Accumulated losses and expenses, which are not actually any virtual assets called as Fictitious Assets. Discount on issue of shares, Profit & Loss account, and capitalized expenditure for time being are the main examples of fictitious assets.

Cash & Cash Equivalents − Cash balance, cash at bank, and securities which are redeemable in next three months are called as Cash & Cash equivalents.

Wasting Assets − The assets, which are reduce or exhausted in value because of their use are called as Wasting Assets. For example, mines, queries, etc.

Tangible Assets − The assets, which can be touched, seen, and have volume such as cash, stock, building, etc. are called as Tangible Assets.

Intangible Assets − The assets, which are valuable in nature, but cannot be seen, touched, and not have any volume such as patents, goodwill, and trademarks are the important examples of intangible assets.

Accounts Receivables − The bills receivables and sundry debtors come under the category of Accounts Receivables.

Working Capital − Difference between the Current Assets and the Current Liabilities are called as Working Capital.

Liability

A liability is the obligation of a business/firm/company arises because of the past transactions/events. Its settlement/repayments is expected to result in an outflow from the resources of respective firm.

There are two major types of Liability −

Current Liabilities − The liabilities which are expected to be liquidated by the end of current year are called as Current Liabilities. For example, taxes, accounts payable, wages, partial payments of long term loans, etc.

Long-term Liabilities − The liabilities which are expected to be liquidated in more than a year are called as Long-term Liabilities. For example, mortgages, long-term loan, long-term bonds, pension obligations, etc.

Grouping of Assets and Liabilities

There may be two types of Marshalling and grouping of the assets and liabilities −

In order of Liquidity − In this case, assets and liabilities are arranged according to their liquidity.

In order of Permanence − In this case, order of the arrangement of assets and liabilities are reversed as followed in order of liquidity.

Financial Statements with Adjustments Entries and their Accounting Treatment

In order to prepare a true and fair financial statement, there are some very important adjustments those have to be done before finalization of the accounts (as shown in the following illustration) −

| Sr.No. | Adjustments | Accounting Treatments |

|---|---|---|

| 1 |

Closing Stock Unsold stock at the end of Financial year called Closing stock and valued at Cost or market value whichever is less |

First Treatment Where an opening and closing stock adjusted through a purchase account and the value of Closing Stock given in Trial Balance − Closing stock will be shown as adjusted purchase account on the debit side of Trading account and will appear in the Balance Sheet under current Assets. |

| 2 |

Outstanding Expenses Expenses which are due or not paid called as outstanding expenses. |

Accounting Treatment Outstanding expenses will be added in Trading or Profit & Loss account in particular expense account and will appear in liabilities side of the Balance Sheet under the current liabilities. |

| 3 |

Prepaid Expenses Expenses which are paid in advance are called as Prepaid Expenses. |

Accounting Treatment Prepaid Expenses will be deducted from the particular expenses as appear in Trading & Profit & Loss account and will be shown in the Balance Sheet under the current assets. |

| 4 | Accrued Income The income, which is earned during the year, but not yet received at the end of the Financial Year is called as Accrued Income. |

Accounting Treatment Accrued income will be added to a particular income under the Profit & Loss account and will be shown in the Balance Sheet as current assets. |

| 5 |

Income Received in Advance An income received in advance, but not earned like advance rent etc. |

Accounting Treatment An income to be reduced by the amount of advance income in profit & loss account and will appear as current liabilities in the Balance Sheet. |

| 6 | Interest on Capital Where an interest paid on the capital introduced by the proprietor or partner of the firm. |

Accounting Treatment

|

| 7 |

Interest on Drawing Where an interest paid on the capital introduced by the proprietor or partner of the firm. |

Accounting Treatment

|

| 8 | Provision for Doubtful Debts If there is any doubt on the recovery from Sundry Debtors. |

Accounting Treatment

|

| 9 |

Provision for Discount on Debtors If there is any offer of discount to pay the debtors within certain period. |

Accounting Treatment

|

| 10 | Bad Debts Unrecovered debts or irrecoverable debts |

Accounting Treatment

|

| 11 |

Reserve for Discount on Creditors If there is any chance to get discount on the payment of sundry creditors within certain period. |

Accounting Treatment

|

| 12 |

Loss of Stock by fire There may be three conditions in this case |

Accounting Treatment 1. If Stock is fully insured

2. If Stock is partially insured

3. If Stock is not insured

|

| 13 |

Reserve Fund |

Accounting Treatment

|

| 14 | Free Sample to Customers |

Accounting Treatment

|

| 15 | Managerial Commission |

Accounting Treatment

|

| 16 | Goods on Sale or Approval Basis If there is any un-approved stock lying with the customers at the end of financial year. |

Accounting Treatment

|

Provision and Reserves

Meaning of Provisions

Any amount written off or retained by the way of providing depreciation or diminution in the value of assets or for providing any known liability of which the amount cannot be determined with substantial accuracy.

- The Institute of Chartered Accountants of India

Liabilities which can be measured only by using a substantial degree of estimation.

- AS-29 issued by Institute of Chartered Accountants of India

AS 29 also defines liabilities as a present obligation of the enterprises arising from past events, the settlement of which is expected to result in an outflow from the enterprise of resources embodying economic benefits.

Debiting Profit and Loss account, provisions are created and shown either deducting assets side or on the liabilities side under relevant sub-head of Balance Sheet.

Provision for bad and doubtful debts, Provisions for Repair & Renewals, and Provision for discounts & depreciation are the most common examples.

Meaning of Reserves

That portion of earnings, receipts or other surplus of an enterprise (whether capital or revenue) appropriated by the management for general or a specific purpose other than a provision for depreciation or diminution in the value of assets or for a known liability.

-ICAI

Reserve is an appropriation of profits; on the other hand, Provision is a charge against profit. Reserves are not meant to meet out contingencies or liabilities of a business. Reserve increases working capital of a company to strengthen the financial position.

There are two types of reserves −

Capital Reserve − Capital reserve is not readily available for distribution as the dividends among the shareholders of the company, and it creates only out of capital profit of the company. It is like Premium on issue of shares or debentures and Profit prior to incorporation.

Revenue Reserve − Revenue reserves are readily available for the distribution of profit as dividend to the shareholders of the company. Some of the examples of this are general reserve, staff welfare fund, dividend equalization reserve, debenture redemption reserve, contingency reserve, and investment fluctuation reserves.

Distinction between Provisions and Reserves

Reserve can be made only out of profit and provisions are the charge to profit.

Reserves reduce divisible profits and provisions reduce the profit.

Reserves, if remain un-utilized for some period can be distributed as dividends, but provisions cannot be transferred to General Reserve for the distribution.

Purpose of provision is very specific, but reserve is created to meet out any probable future liabilities or losses.

Creation of provisions is legally necessary, but reserves are created to save a concern from the future losses and liabilities.

Secret Reserves

Banking Company, Insurance Company, and Electricity Companies create secret reserves, where the public confidence is required. In this case, to create secret reserve, assets showed at lower cost or liabilities at higher value. Some of the examples of it are as follows −

- By undervaluing goodwill or stock

- By excessive depreciation

- By creating excessive provisions

- Showing free reserves as creditors

- By charging capital expenditure to profit and loss account

Advantages of Secret Reserves

Some of the important advantages are given below −

Without disclosing to its shareholders, it increases working capital of a concern, which is a clear indication of the sound financial position.

With the help of secret reserves, directors can maintain the rate of dividends during the unfavorable time.

Non-disclosure of a big profit is useful to avoid an un-due competition.

Limitations of Secret Reserves

Major limitations or objections of secret reserves are as follows −

Due to non-disclosure of actual profit, financial statements do not presents true and fair view of the state of affairs.

There are lots of chances of misuse of reserves by the directors for their personal benefits.

Due to secret reserves, chances for the concealment of worst position of a company are very high.

Company will get very lower amount of claim of insurance at the time of loss of stock or other assets, as valuation of the assets are done at very low value to create secret reserve.

General and Specific Reserves

Specific reserves are created and utilized for the purpose only for which they are created, like dividend equalization reserve and debenture redemption reserve.

General reserves are created for any future contingency or to utilize at the time of expansion of a business. Purpose of creation of General reserve is to strengthen the financial position of the company and to increase the working capital.

Sinking Fund

For the purpose to repay of any liabilities or to replace any fixed assets after particular period, sinking funds are created. For this, some amount are charged or appropriated from the profit and loss account every year and invested in any outside securities. Without any extra ordinary burden, replacement of an asset may be done in a systematic manner or pay any known liability on maturity of the sinking fund.

Investment of Reserves

It is a controversial issue, whether a reserve should be invested in outside securities or not. Thus, to decide anything, it is important to study the need and requirement of a firm according to the financial position of a firm. Therefore, investment in outside securities is justified only in a case where company has the extra fund to invest.

Nature of Reserve

In-spite of showing reserves on the liabilities side of a Balance Sheet, reserves are actually not at all any liabilities of a firm. Reserve represents as accumulated profits, which are available to disburse among the shareholders.

Measurement of Business Income

One of the most significant accounting concepts is Concept of Income. Similarly, measurement of a business income is also an important function of an accountant.

In General term, payment received in lieu of services or goods are called income, for example, salary received by any employee is his income. There may be different type of incomes like Gross income, Net income, National Income, and Personal income, but we are here more concerned for a business income. Surplus revenue over expenses incurred is called as Business Income.

Objectives of Net Income

Following are the important objectives of a net income −

Historical income figure is the base for future projections.

Ascertainment of a net income is necessary to give portion of profit to employees.

To evaluate the activities, which give higher return on scarce resources are preferred. It helps to increase the wealth of a firm.

Ascertainment of a net income is helpful for paying dividends to the shareholders of any company.

Return of income on capital employed, gives an idea of overall efficiency of a business.

Definition of Income

The most authentic definition is given by the American Accounting Association as −

The realized net income of an enterprise measures its effectiveness as an operative unit and is the change in its net assets arising out of a (a) the excess or deficiency of revenue compared with related expired cost, and (b) other gains or losses to the enterprise from sales, exchange or other conversion of assets:.

According to the American Accounting Association, to be as business income, income should be realized. For example, to be a business income, only appreciation in value of assets of a company is not enough, for this, asset has really been disposed of.

Accounting Period

For the measurement of any income concerns, instead of a point of time, a span of time is required. Creditors, investors, owners, and government, all of them require systematic accounting reports at regular and proper intervals. The maximum interval between reports is one year, as it helps a businessman to take any corrective action.

An accounting period concept is directly related to matching concept and realization concept; in the absence of any of them, we could not measure income of the concerns. On the basis of matching concept, expenses should be determined in a particular accounting period (usually a year) and matched with the revenue (based on realization concept) and the result will be income or loss of the accounting period.

Accounting Concept and Income Measurement

The measurement of accounting income is the subject to several accounting concepts and conventions. Impact of accounting concepts and convention on measurement of the accounting income is given below −

Conservatism

Where an income of one period may be shifted to another period for the measurement of income is called as conservatism approach.

According to the convention of conservatism, the policy of playing safe is followed while determining a business income and an accountant seeks to ensure that the reported profit is not over stated. Measurement of a stock at cost or market price, whichever is less is one of the important examples as applied to measurement of income. But it must be insured that providing excessive depreciation or excessive provisions for a doubt full debt or excessive reserve should not be there.

Consistency

According to this concept, the principle of consistency should be followed in accounting practice. For example, in the treatment of assets, liabilities, revenues, and expenses to insure the comparison of accounting results of one period with another period.

Therefore, the accounting profession and the corporate laws of most of the counties require that financial statement must be made out on the basis that the figures stated are consistent with those of the preceding year.

Entity Concept

Proprietor and business are the two separate and different entities according to the entity concept. For example, an interest on capital is business expenditure, but for a proprietor, it is an income. Thus, we cannot treat a business income as personal income or vice-versa.

Going Concern Concept

According to this concept, it is assumed that business will continue for a long time. Thus, charging depreciation on a Fixed Asset is based on this concept.

Accrual Concept

According to this concept, an income must be recognized in the period in which it was realized and costs must be matched with the revenue of that period.

Accounting Period

It is desirable to adopt a calendar year or natural business year to know the results of business.

Computation of Business Income

To compute business income, following are the two methods −

Balance Sheet Approach

Comparison of the closing values (Assets minus outsiders liabilities) of a firm with the values at the beginning of that accounting period is called as Balance Sheet approach. In above value, an addition to capital will be subtracted and addition of drawings will be added while computing the business income of a firm. Since, income is calculated with the help of Balance Sheet hence called as Balance Sheet approach.

Transaction Approach

Transactions are mostly related to production or the purchase of goods and the sale of goods and all these transactions directly or indirectly related to the revenue or to the cost. Therefore, surplus collection of the revenue by selling goods, spent over for production or purchasing the goods is the measure of income. This system is widely followed by the enterprises where double entry system adopted.

Measurement of Business Income

There are following two factors which are helpful in the estimation of an income −

Revenues − Sale of goods and rendering of services are the way to generate revenue. Therefore, it can be defined as consideration, recovered by the business for rendering services and goods to its customers.

Expenses − An expense is an expired cost. We can say the cost that have been consumed in a process of producing revenue are the expired cost. Expenses tell us - how assets are decreased as a result of the services performed by a business.

Measurement of Revenue

Measurement of the revenue is based on an accrual concept. Accounting period, in which revenue earned, is the period of revenue accrues. Therefore, a receipt of cash and revenue earned are the two different things. We can say that revenue is earned only when it is actually realized and not necessarily, when it is received.

Measurement of Expenses

In case of delivery of goods to its customers is a direct identification with the revenue.

Rent and office salaries are an indirect association with the revenue.

There are four types of events (given below) that need proper consideration about as an expense of a given period and expenditure and cash payment made in connection with those items −

Expenditure, which are expenses of the current year.

Some expenditure, which are made prior to this period and has become expense of the current year.

Expenditure, which is made this year, becomes expense in the next accounting periods. For example, purchase of fixed assets and depreciation in next up-coming years.

Expense of this year, which will be paid in next accounting years. For example, outstanding expenses.

Matching Concept

It is a problem of recognition of revenue during the year and allocation of expired cost to the period.

Recognition of Revenue

Most frequent criteria, which are used in recognition of the revenue are as follows −

Point of Sale − Transfer of ownership title to a buyer is point of sale, in case of sale of commodity.

Receipt of Payment − Criteria of cash basis is widely used by the attorneys, physicians, and other professionals in which revenue is considered to be earned at the time of collection of cash.

Instalment Method − Instalment method is widely used in retail trading specially in consumer durables. In this system, revenue earned is treated in the same manner as is used in any other credit sale.

Gold Mines − The accounting period in which gold is mined is the period of revenue earned.

Contracts − Degree of contract completion, especially in long term construction contracts is based on percentage of completion of a contract in a single accounting year. It is based on total estimated life of the contract.

Allocation of Costs

Matching of expired revenue and expired costs on a periodic time basis is the satisfactory basis of allocation of cost as stated earlier.

Measurement of Costs

Measurement of costs can be determined by −

Historical Costs − To determine periodic net income and financial status, historical cost is important. Historical cost actually means - outflow of cash or cash equivalents for goods and services acquired.

Replacement Costs − Replacing any asset at the current market price is called as replacement cost.

Basis of Measurement of Income

Following are the two significant basis of measurement of income −

Accrual Basis − In an accrual basis accounting, incomes are recognized in a companys books at the time when revenue is actually earned (however, not essentially received) and expenses is recorded when liabilities are incurred (however, not essentially paid for). Further, expenses are compared with revenues on the income statement when the expenses expire or title has been transferred to the buyer, and not at the time when the expenses are paid.

Cash Basis − In a cash basis accounting, revenues and expenses are recognized at the time of physical cash is actually received or paid out.

Change in the Basis of Accounting

We have to pass adjustment entries whenever accounting records change from cash basis to accrual basis or vice versa specially in respect of the prepaid expenses, outstanding expenses, accrued income, income received in advance, bad debts & provisions, depreciation, and stock in trade.

Features of Accounting Income

Followings are the main features of accounting income −

Matching revenue with related cost or expenses is a matter of accounting income.

Accounting income is based on an accounting period concept.

Expenses are measured in terms of a historical cost and determination of expenses is based on a cost concept.

It is based on a realization principal.

Revenue items are considered to ascertain a correct accounting income.

Bills of Exchange and Promissory Notes

An Instrument in writing containing an unconditional order, signed by the maker, directing a certain person, to pay a certain sum of money only to, or to the order of a certain person or to the bearer of the instrument.

Section 5, Negotiable Instrument Act, 1881

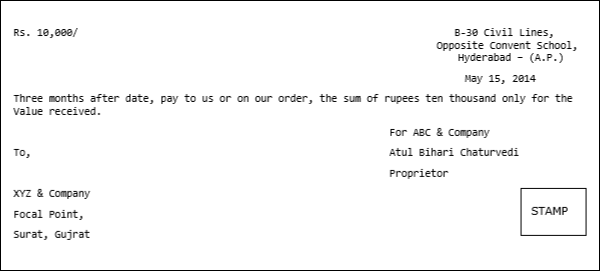

Essentials of Bills of Exchange

Following are the essentials of a bill of exchange −

Bill of exchange should be in written.

The seller who makes the bill is termed as Drawer, the purchaser upon whom the bill is drawn is known as Drawee and must be a person.

Bill of exchange must be carrying certain amount and only in terms of money, and not in terms of goods or services.

Order to pay the money, should be unconditional.

Specimen of Bill

Apart from all these (given above), we also need to pay attention on the following points −

Parties to Bill of Exchange

Following are the parties of Bill of Exchange −

The Drawer − Seller of goods is termed as drawer of bills of exchange.

The Drawee − Drawee or purchaser is a person who accepts the bill of a certain amount to be paid after a specific time.

The Payee − Payee and drawer may be same person who gets the payment or may be a different person. In case of same parties, will be reduced to two instead of three.

Important Terms

Stamp − Amount in excess of certain limit should be paid and signed on affixed revenue stamp according to above specimen. In these days, threshold limit is INR 5,000/.

Amount − Amount of bill must be written in figure as well as in words as shown in above specimen.

Date − Date on bill will be written on face of it as above.

Value and Terms − Both are essential part of it and must be written as shown above.

Acceptance of Bills

To make it a legal document, it must be signed by Drawee. Acceptance may be general acceptance i.e. Drawee agrees with the full content of the bill without any change and it may be conditional, which is called as qualified acceptance.

Classification of Bills of Exchange

Bill of exchange may be classified as viz

Inland Bill − Bill, which is drawn in India, both the Drawer and the Drawee are from India and also payable in India called Inland Bill.

Foreign Bill − Bill, which is drawn outside India, drawn on a person residing in India, payable in India or vice versa. Due date of foreign bill starts from the date on which Drawee sees it and accepts it.

Definition of Promissory Notes

As per Section 4 of the Indian Negotiable Instrument Act, 1881

An instrument in writing (not being a Bank note or a currency note) containing an unconditional undertaking, signed by the maker, to pay a certain sum of money only to, or the order of a certain person, or to the bearer of the instrument.

Difference between Promissory Notes and Bills of Exchange

| Promissory Note | Bill of Exchange |

|---|---|

| It is an unconditional promise to pay | Bill of Exchange is unconditional order to pay. |

| Debtor make the promise to pay to the creditor | Bill of Exchange drawn by a seller of goods or services and he makes an order to debtor to make the payment. |

| Foreign promissory note make in a set of one only | Foreign Bills of Exchange drawn in a set of three. |

| Promissory note payable on demand, requires stamp duty | Bill of Exchange payable on demand does not require stamp duty. |

| Promissory note has only two parties i.e. drawer and payee | Bill of exchange may have three parties, drawer, drawee and may be payee. |

| Since debtor himself makes the promise to make the payment, hence no acceptance required in this case | To be a legal document, it must be accepted by Drawee. |

Advantages of Bills of Exchange and Promissory Notes

Followings are the important advantages of Bills of Exchange and Promissory Notes −

Facilitation of the credit transactions is helpful in increasing the size of business.

Both are the proof of purchase of goods or services in credit.

Being a legal document, both can be produced in a court, in case of its dishonor.

Since date of payment is fixed, it is helpful for both debtors and creditors; and, they may manage their payment schedule accordingly.

In case of any urgency of payment, creditor can get the bill discounted from the bank.

Being a negotiable instrument, promissory note is easily transferable from one person to another.

Accounting Treatment

Bills of exchange and Promissory notes are treated as bills receivable and bills payable in regards to accounting treatment −

Bills Receivable − If we have to receive the payment against bills of exchange or promissory note, it will be called as Bills Receivable and will be shown in the Asset side of Balance-sheet under Current Assets.

Bills Payable − Bills payable is current liabilities in hand of Drawee.

Accounting Entries − When the Bill received and retained in possession till due date.

Accounting entries to be done in the books of Drawer and Payee as −

| Sr.No. | In the Books of Drawer | Entries in the Books of Acceptor |

|---|---|---|

| 1 | Customer A/cDr To Sales A/c (Being Goods sold on credit) |

Goods Purchase A/cDr To Supplier A/c (Being Goods Purchased on credit) |

| 2 | Bills Receivable A/cDr To Customer A/c (Being Bill accepted by Customer) |

Supplier A/cDr To Bills Payable A/c (Being Bill accepted drawn by supplier of goods) |

| 3 | Cash/Bank A/cDr To Bills Receivable A/c (Being Amount of bill received on due date) |

Bills Payable A/cDr To Cash/Bank (Being Amount paid on due date and bills payable received back) |

When Bill is Discounted with the Bank

In the Book of Drawer − The drawer of a bill may get the bill discounted from his bank before due date of that bill. In this case, bank charges some interest on bill amount according to waiting time. For example, if bill is drawn on 1st January for 3 months and drawer may get bill discounted on 1st February, in this case, bank will charge interest for two months at applicable rate say 14% and drawer of bill may pass following entry.

Cash / Bank A/c Dr Discount A/c Dr To bills Receivable A/c (Being bill discounted with bank @ 14% p.a. discount charge debited by bank for 2 months)

In the book of Drawee − Drawee has no need to pass entry on above, he just needs to pass the entry at the time of payment on maturity of bill as explained earlier.

When Bill of Exchange Endorsed in Favor of a Creditor

If Drawer of the bill of exchange endorsed the bill to his creditor for his own liabilities and bill is met on maturity, following journal entries will be passed −

In the book of Drawer

Creditors A/c Dr To bills Receivable A/c (Being bill receivable endorsed to creditor)

Note − Drawer has no need to pass any entry at the time of maturity of a Bill.

In the book of Drawee − Drawee has no need to pass any entry at the time of endorsement of Bill. Entries will remain same as explained earlier.

Dishonor of a Bill of Exchange

In case where the acceptor of a Bill of Exchange failed to pay the bill on due date of maturity or refused to pay, it is called as dishonor of a Bill of Exchange. As a proof of dishonor of a Bill, payee may get a certificate from a Notary Officer appointed by the Government for this purpose. Notary officer charges some fees in this regard called as Noting Charges.

Following entries will pass in the books of Drawer and Drawee −

| Sr.No | In the Books of Drawer |

|---|---|

| 1 | If bill is kept by the Drawer with himself till the date of maturity − Customer/Acceptor A/c Dr (with total Bill amount + Noting Charges) To Bills Receivable A/c(with Bill Receivable amount) To Cash/Bank(Noting Charges paid) (Being Bills receivable dishonor and noting charges paid) |

| 2 | If bill is discounted with the bank − Customer/Acceptor A/c Dr (with total Bill amount + Noting Charges) To Bank A/c(with total Bill amount + Noting Charges) (Being discounted Bills receivable dishonor and noting charges paid) |

| 3 | If bill is endorsed by the Drawer in favor of a Creditor − Customer/Acceptor A/c Dr (with total Bill amount + Noting Charges) To Creditor A/c(with total Bill amount + Noting Charges) (Being endorsed Bills receivable dishonor and noting charges paid) |

| Entries in the Books of Acceptor/Debtors |

|---|

|

In all above three case acceptor will pass only one journal entry − Bills payable A/cDr(with the bills payable amount) Noting Charges A/cDr(with Noting Charges ) To Drawer/Creditor A/c(with total Bill amount + Noting Charges) (Being Goods Purchase on credit) |

Renewal of Bill

There may be a situation when the acceptor of bill may not be in position to pay the bill on due date and he may request drawer to cancel the old bill and draw a new bill on him (i.e. Renewal of Bill). Drawer of bill may charge some interest on mutually agreed terms and that amount of interest may be paid in cash or may be included in the bill amount.

Entries in the Books of Drawer and Drawee

Following accounting entries to be done in the books of Drawer and Drawee −

| Sr.No. | In the Books of Drawer | Entries In the Books Acceptor |

|---|---|---|

| 1 | Cancellation of old bill − Customer/Acceptor A/cDr To Bill receivable A/c (Being old bill cancelled) |

Cancellation of old bill − Bills Payable A/cDr To Creditor A/c (Being request for cancellation of old bill accepted by Creditor) |

| 2 | Interest received in cash − Cash A/cDr To Interest A/c (Being interest received on delayed payment) |

Interest paid in cash − Interest A/cDr To Cash A/c (Being Interest paid on renewal of Bill) |

| 3 | In case interest not payable in cash − Customer/Acceptor A/cDr To Interest A/c (Being Interest due on renewal of bill) |

In case interest not payable in cash − Interest A/cDr To Creditor A/c (Being Interest on renewal of bill due) |

| 4 | On renewal of bill − Bills Receivable A/cDr To Customer/Acceptor A/c (Being renewal of bill including amount of interest) |

On renewal of bill − Supplier A/cDr To Bills Payable A/c (Being Bill accepted after cancellation of a new bill including interest) |

Retiring of a Bill under Rebate

Sometimes, acceptor may approach to drawer of a bill to make early payment before due date of a bill, following journal entries will pass in this case −

| Sr.No. | Entry In the Books of Drawer | Entries In the Books of Acceptor |

|---|---|---|

| 1 | Cash/Bank A/cDr Rebate A/cDr To Bills Receivable A/c (Being Amount of bill received before due date and rebate allowed to customer) |

Payable A/cDr To Cash/Bank A/c To Rebate A/c (Being Amount paid before due date on rebate) |

Bill sent to Bank for Collection

To manage several numbers of bills receivable, drawer sent those bills to the bank for collection and bank gives credit to the customer whenever a bill is collected from a drawee. Following journal entries will be passed −

| Sr.No. | Entry In the Books of Drawer |

|---|---|

| 1 | When a bill is sent to the bank for collection − Bills sent for Collection A/cDr To Bank A/c (Being bills receivable sent to the bank for collection) |

| 2 | On collection of payment by bank − Bank A/cDr To Bills sent for Collection A/c (Being Collection of bills receivable by bank) |

Accommodation Bill

A bill of exchange may be accepted to oblige a friend or any known person at the time of his need or to provide him a loan or else to accommodate one or more parties is called as accommodation bill.

Financial Accounting - Inventory Valuation

The Institute of Chartered Accountant of India as per Accounting Standard-2 (Revised) defines inventory as the assets held −

For sale in the ordinary course of a business or

In the process of production for such a sale or

In the form of materials or supplies to be consumed in the production process or in rendering of the services.

Thus, the term inventory includes −

- Raw Material and supplies,

- Work in progress, and

- Finished goods.

Importance of Inventory Valuation

Proper valuation of inventory is important because of the following three reasons −

Importance of sufficient Inventory − An inventory represents major current asset investment of any trading or manufacturing concern. Shortage of inventory may close down the business. Realization of profit from resale of an inventory makes valuation of inventory. Therefore, the point is that every business unit has to follow a proper method of inventory valuation.

To Determine True Financial Position − Proper valuation of an inventory can only give true and fair view of the financial position of a business unit, as it constitutes a significant portion of the current assets.

For Proper Determination of Income − Proper determination of income and profit depends on correct valuation of the inventories. Over valuation of closing inventory may overstate the profit figure and vice-versa. Therefore, proper valuation of an inventory is necessary to determine the true income and profit by the business concern.

Methods of Taking Inventory

Following are the two important methods of taking inventory −

- Periodic Inventory Method and

- Perpetual Inventory Method

Lets discuss each of them separately −

Periodic Inventory Method

This method of stock valuation is also known as physical stock taking method or annual stock taking method. Under this system of taking inventories, stock is determined by physical counting at the end of the accounting period i.e. the date of preparation of final accounts. This system is very simple and useful in small business organizations.

Perpetual Inventory Method

This system of inventory valuation records every movement of stock on the receipt and issue of material reflecting running balances of different kind of inventories through preparation of store ledgers for raw material, work-in- progress, and finished goods. To insure the accuracy of store records, a periodic reconciliation of records is done by taking physical inventories.

Valuation of Inventory at Lower Cost or Market Price

An inventory is valued at a cost or market price, whichever is lower to ensure that the anticipated profit should not be accounted for and full provision for anticipated losses should be done.

As per American Institute of Certified Public Accountants −

A departure from the cost basis of pricing the inventory is required when the utility of the goods is no longer as great as its cost. Where there is evidence that the utility of goods, in their disposal in the ordinary course of business, will be less than cost, whether due to physical deterioration, obsolescence, changes in price levels, or other causes, the difference should be recognized as loss of the current period. This is generally accomplished by stating such goods at a lower level commonly designated as market.

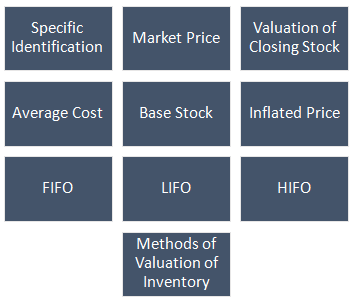

Methods of Valuation of Inventory

The following illustration shows the methods of Valuation of Inventory −

Lets discuss each one of the methods in detail.

First in First out (FIFO) Method

FIFO is the most popular method of an inventory valuation, which is based on assumption that the material first received or purchased are the first to be sold or issued. It means, closing stock is out of the last or latest received or manufactured goods.

It will clear with a small and simple example as given below −

| Date | No. of Item | Rate | Value |

|---|---|---|---|

| Opening stock | 100 | 10 | 1000 |

| Purchased on 01-04-13 | 500 | 10 | 5000 |

| Purchased on 01-07-13 | 500 | 12 | 6000 |

| Purchased on 01-01-14 | 1000 | 15 | 15000 |

| Total Purchases | 2100 | 27000 | |

| Item Sold | 1700 | ||

| Closing stock | 400 | 15 | 6000 |

In above example, it is assumed that closing stock of 400 items was out 1000 items purchased on 01-01-2014.

Last in First out (LIFO) Method

As name suggests, closing stock is valued on the basis of oldest purchased or manufactured items. First time, this method was used by the U.S.A., at the time of Second World War to get the advantage of hike in prices. In the above example, closing stock will be valued at 400 items @ Rs. 10 each = Rs. 4000

Note − Here 100 items from opening stock and 300 items were out of purchases made on 01-04- 2013

Average Cost Method

Average cost method is used where identification of stock with rate or value of stock is not possible. It is of two types Viz

- Simple Average Price Method

- Weighted Average Price Method

Simple Average Price Method

Simple average price method may be explained as below −

Suppose, four types of items are in stock as follows −

| 500 units purchased @ Rs. 10 per unit | = Rs. 5000 |

| 750 units purchased @ Rs. 12 per unit | = Rs. 9000 |

| 600 units purchased @ Rs. 14 per unit | = Rs. 8400 |

| Total Units 1850 for | = Rs. 22400 |

Simple average method ignored the inventory at cost, therefore the valuation of stock of 1850 units will be = 12 × 1850 = Rs. 22,200 whereas the actual cost is Rs. 22,400

So, if we want to choose average method then weighted price method should be followed under which valuation will be done as hereunder.

Weighted Average Price Method

In the above example, Rs. 22,400 will be divided by 1850 units and the average price will be Rs. 12.1081.

Highest in First out (HIFO) Method

This method is based on the assumption that the highest value of material always consumed first and closing stock will be valued at the lowest cost of purchased or manufactured material. This method is not a popular method of valuation of inventory and so, used only by the business units having monopoly products or who are dealing with the cost + contract.

Base Stock Method

Base stock means minimum level of stock maintained by a business unit to run his business without any interruption or which is according to AS-2 issued by The Institute of Chartered Accountants of India as the base stock formula proceeds on the assumption that a minimum quantity of inventory (base stock) must be held at all times in order to carry on business.

Note − This method can be followed only when LIFO method is used.

Inflated Price Method

This method of valuation covers normal losses, increasing price of purchases to calculate closing value of an inventory. For example, if 550 units purchased for Rs. 2000 and due to normal loss units, remain 500 then the cost per unit will be 2000/500 = Rs. 4 per unit, and while calculating closing stock value for 100 unit, cost will be Rs. 400 (100 × 4).

Specific Identification Method

Under this method, where identification of items with price is possible, then closing stock will be valued accordingly.

Market Price Method

Under this method of valuation, stock is valued at current market price. It is also called replacement price or realizable price method.

Method of Valuation of Closing Stock when it is not given

In case, where the value of closing stock is not given, we may calculate it as −

| Opening stock | xx |

| Add: Net Purchases | xx |

| Less: Cost of Sales | xx |

| Less: Gross Profit | xx |

| Value of Closing stock | xx |

Putting value in above formula, we may also calculate the value of opening stock.

Analysis of Changes in Income

The purpose of preparing a financial statement is not only to know the net income or losses of concern for the current year, but also to know the change in net income or losses of a firm in comparisons to the preceding years.

There are two types of financial statements, which reflect two types of profits i.e. trading account shows the gross profit and Profit & Loss accounts shows the net profit of the concern for a specific accounting period. Under this chapter, we will discuss the reasons for changes in Gross Profit Ratio.

Gross Profit Ratio (GPR)

Gross profit means, excess of sales over cost of goods sold. This ratio also indicates the losses due to damage or mismanagement. More the ratio is high more it is good for a financial health of a concern. Chances of higher net income are more in an organization where ratio of gross profit is high (formula is given below) −

$$\normalsize Gross\:Profit\:Ratio = \frac{Gross\:Profit}{Net\:Sales}$$

Higher gross profit provides leverage to the management to meet their indirect expenses and to spare net income for the distribution of profit and to increase the reserves.

Gross Profit Margin

When Gross profit margin is presented in percentage, it is called as Gross profit margin (formula is given below) −

$$\normalsize Gross\:Profit\:Margin = \frac{Gross\:Profit}{Net\:Sales} \times 100$$

Chances of Increase in GPR may be due to following Reasons −

Without increase in corresponding costs, if there is an increase in selling price.

Without decrease in selling price, if there is decrease in cost of production of products.

There may be equal decrease or increase in selling price and cost of production without affecting gross profit of the current year.

There may be chances that the valuations of closing stocks are done with higher price.

It is also possible that the opening stock of a concern is valued at very lower rate.

There is a possibility that given sales are inclusive of consignment sale due to any mistake or otherwise.

Omission of purchase invoices in the books of accounts may also be one of the reasons for higher gross profit.

Chances of Decrease in GPR may be due to following Reasons −

- If cost price remains same, but decrease in selling price.

- Sale price remains same, but increase in cost of production.

- Personal used goods debited to purchase account.

- Closing stock may be valued at very low price.

- Opening stock may be valued at very high price.

- Any omission or mistake while valuation of closing stock.

It is necessary for survival and progress of any business to keep its margin of gross profit high as much as possible to enable it to cover its operative expenses as well as indirect expenses.

Analysis of Gross Profit

Analysis of changes in gross profit is the first step in determination of a net income. Change of gross profit in current year may be due to the following reasons −

- Change in sale amount may be due to following three reasons −

- Change in selling price.

- Change in quantity sold without change in sale price.

- Change in sale price as well as quantity of goods sold.

- Change in cost of goods sold may be due to following reasons −

- Change in cost of production.

- Change quantity of goods sold.

- Change in quantity as well as cost of goods sold.

Example

Make an analysis of changes from the information given below −

| Particulars | Year 2012 (Rs.) | Year 2013 (Rs.) | Changes (Increase or decrease) |

|---|---|---|---|

| Sales | 3,50,000 | 4,80,000 | 1,30,000 |

| Number of Unit sold | 5,000 | 6,000 | 1,000 |

| Selling Price per Unit | 70 | 80 | 10 |

Solution

Increase in sales amount due to price −

Increase in price per unit × Number of unit sold in current year

= 10 × 6000 = 60,000

Increase in sales amount due to Quantity −

Increase in number of unit sold × price of last year

= 1,000 × 70 = 70,000

Combined effect of change in quantity and price (A+B)

= 1, 30,000

Accounting for Consignment

Due to increasing size of market, it is quite obvious that manufacturers or whole sellers cannot approach directly to every customer around the state or nation. To overcome this limitation, manufacturers normally appoint reliable agents at every desired location to reach the customers directly. He makes an agreement with local traders who can sell goods on his behalf on commission basis.

Meaning and Features of Consignment

Consignment is a process under which the owner consigns/handovers his materials to his agent/salesman for the purpose of shipping, transfer, sale etc.

Following are the points that throw more light on the nature and scope of a consignment −

Here, ultimate ownership of the goods remains with the manufacturer or whole seller who handovers goods to his agent for sale on commission basis. Consignment is merely a transfer of possession of goods not an ownership.

Since ownership of goods remain with the manufacturer (consignor), consignee (agent) is not responsible for any loss or destruction of goods.

The goods are sold on owners risk and hence, profit/loss goes to owner.

Consignee only gets re-imbursement of expenses incurred by him and commission on sale made by him, because sale that proceeds, belongs to owner (consignor).

Why is Consignment not a Sale?

Following are the reasons that explain why consignment is not a sale −

Ownership − Ownership of goods need to be transferred from seller to buyer in case of sale, but ownership of goods remains with the consignor, till the goods are sold by the consignee.

Risk − In case of a consignment, normally, risk remains with the consignor in the event of goods being lost or destroyed.

Relationship − The relation between a seller and a buyer will be of debtor and creditor in case where goods are sold on credit basis. On the other hand, the relationship between a consignor and a consignee is that of principal and agent.

Goods Return − Usually, the sold goods cannot be returned back; however, if there is any manufacturing defect or any other technical fault, seller is obliged to take them back. On the other hand, consignee may return the unsold stock of goods to consignor anytime.

Important Terms

Pro-forma Invoice

Invoice implies that the sale has taken place, but pro-forma invoice is not an invoice. Proforma invoice is a statement prepared by the consignor of goods showing quantity, quality, and price of the goods. Such pro-forma invoice is issued by the consignor to consignee regarding the goods before the sale actually takes place.

Account Sale

Statement showing the details of goods received, goods sold, expenses incurred, commission charged, remittances made, and due balance is called Account Sale and it is remitted by the consignee to the consignor of goods on a periodic basis.

Commission

There are three types of commission payable to consignee on sale of the goods −

Simple Commission − This is usually a fixed percentage on the total sale, calculated as per mutually agreed terms.

Over-riding Commission − In case of an extra-ordinary sale of the goods, some specific amount is payable to consignee in the form of an incentive is called overriding commission. Over-riding commission is also calculated on the total sales.

Del-credere Commission − An agreement by which an agent or factor, in consideration of an additional premium or commission (called a del credere commission), engages, when he sells goods on credit, to insure, warrant, or guarantee to his principal the solvency of the purchaser, the engagement of the factor being to pay the debt himself if it is not punctually discharged by the buyer when it becomes due.

C. & G. Merriam Co.

A del credere commission is paid by the consignor to his agent for taking additional risk of recovery of debts from the consignee on an account of credit sales made by him (agent) on consignor's behalf.

Direct Expenses

Expenses, which increases the cost of the goods and are of non-recurring nature and incurred till the goods reach the warehouse of consignee may called direct expenses.

Indirect Expenses

Warehouse rent, storage charges, advertisement expenses, salaries, etc. comes under the category of the indirect expenses. The distinctions between direct and indirect expenses are important especially at the time of valuation of the unsold closing stock.

Advance

Amount paid in advance by a consignee to consigner as security called as advance.

Valuation of unsold Consignment

Valuation of unsold stock will be done like a closing stock of a Trading concern and should be valued at the cost or the market price whichever is low. This stock will be valued at −

- Proportionate cost price and

- Proportionate direct expenses.

Here, proportionate direct expenses mean all expenses incurred by the consignor and the expenses of consignee, which are incurred by him till the goods reach the warehouse.

Invoicing Goods higher than Cost

Under this method, goods are charged at the cost + profit and the pro-forma invoice also shows this higher price of such goods. To know the actual profit, at the end of an accounting period, consignment account will be credited with excess price so charged. Value of the stock will also be adjusted to the extent of profit element. Main reason to adopt this policy by consignor is −

To hide actual profit from consignee.

Valuation of a stock at the consignors warehouse is comparatively easy in this case.

In this case, consignor usually directs consignee to sale goods on invoice price only. It prevents different sale price to different customers.

Loss of Goods

There may be two types of losses as explained below −

Normal Loss − Normal loss may occur due to inherent characteristics of goods like evaporation, drying up of goods, etc. It is not separately shown in the consignment account, but included in the cost of goods sold and the closing stock by inflating the rate per unit. To calculate the value of unsold stock, following formula is used.

$$\small Value\:of\:closing\:stock = \frac{Total\:value\:of\:goods\:sent}{Net\:quantity\:received\:by\:consignee} \times Unsold\:quantity$$

$$\small Net\:quantity\:received = Goods\:consigned\:quantity - Normal\:loss\:quantity$$

Abnormal Loss − An abnormal loss may occur due to any accidental reason. It is credited to the consignment account to calculate actual profitability. Valuation of closing stock is done on the same basis as explained earlier i.e. proportionate cost + proportionate direct expenses.

Abnormal Loss and Insurance

If, there is an insurance policy in respect of the consigned goods; following entries will be passed in the books of a consignor −

| Sr.No. | In the Books of Consignor | In the Books of Consignee |

|---|---|---|

| 1 |

Payment of Insurance Premium (a) If insurance premium is paid by the consignor, then cash will be credited. (b) If Insurance premium is paid by the consignee, then consignees A/c will be credited. |

Consignment A/cDr To Cash A/c Or To Consignee A/c (Being Insurance premium paid) |

| 2 | At the time of Abnormal Loss |

Abnormal Loss A/cDr To Consignment A/c (Being Loss Incurred) |

| 3 | Acceptance of Claim by Insurance Company |

Insurance Company (Name of the insurer) A/cDr To Abnormal Loss A/c (Being claim admitted) |

| 4 | On receipt of Claim |

Bank A/cDr To Insurance Company A/c (Being amount of claim received) |

| 5 | In Case of Loss |

Profit & Loss A/cDr To Abnormal Loss A/c (Being amount of Abnormal Loss transferred) |

Summary of Accounting Entries

Following Accounting Entries (Except for Loss) will be done in the books of consignor and consignee for transactions related to the consignment −

| Sr.No. | In the Books of Consignor | In the Books of Consignee |

|---|---|---|

| 1 | When goods are sent to the consignee Consignment A/cDr To Goods Sent on Consignment A/c (Being Goods Sent on Consignment) |

No need to do any Entry in this case |

| 2 | Expenses Incurred by Consignor Consignment A/cDr To Cash/Bank A/c (Being Expenses incurred on consignment) |

Not Applicable |

| 3 | Advance given by consignee Cash/Bank A/cDr To Consignees A/c (Being advance received from consignee) |

Consigner A/cDr To Bank/Cash A/c (Being Advance amount paid to Consignor) |

| 4 | Expenses Incurred by Consignee Consignment A/cDr To Consignees A/c (Being Expenses incurred by consignee) |

Consigner A/cDr To Bank/Cash A/c (Being Expenses incurred on goods received on consignment) |

| 5 | Sale by Consignee Consignees A/cDr To Consignment A/c (Being Expenses incurred by consignee) |

Cash (for cash sale) A/cDr Debtors (for Credit Sale) A/c Dr To Consignor A/c (Being goods sold) |

| 6 | Commission to Consignee Consignment A/cDr To Consignees A/c (Being Commission on sale due to consignee) |

Consigner A/cDr To Commission A/c (Being Commission earned) |

| 7 | Remittance from Consignee Cash/Bank A/cDr To Consignees A/c (Being due amount received from consignee) |

Consigner A/cDr To Bank/Cash A/c (Being Balance due Payment made to consignor) |

| 8 | Entry for Profit on Consignment Profit & Loss A/cDr To Consignment A/c (Being Profit earned on consignment) |

Not Applicable |

| 9 | Loss on Consignment Consignment A/cDr To Profit & Loss A/c (Being Loss incurred on Consignment transferred to the profit & Loss Account) |

Not Applicable |

Note − The goods sent on consignment account will be closed by transferring balance into the Purchase account or the Trading account.

Financial Accounting - Joint Venture

An association of two or more persons or we may say temporary partnership combined for the carrying out a specific business, and divide profit or loss thereof in agreed ratio is called a Joint Venture. Concerned parties to joint venture are known as co-venturers. The liabilities of co-venturers are limited to their profit sharing ratio or as per agreed terms −

Suppose A and B undertake the job to develop a park for a consideration of Rs. 50,000/- Lacs. Since they come together for a work on a specific project, it will termed as joint venture and each of them (A and B) will be called as a co-venturer. Further, this venture will automatically terminate once the project is completed.

Major Features and Characteristics of Joint Venture

Following are the major features of a joint venture −

There is an agreement between two or more persons.

Joint venture is made for the specific execution of a business plan/project.

It is a temporary partnership without the use of a firm name.

Agreement for joint ventures is automatically dissolved as soon as specific project is over.

Profit & Share are shared on the same terms and conditions agreed upon. However, in the absence of any agreement, profit & share will be divided equally.

Partnership and Joint Venture

There are following differences between partnership and joint venture −

Partnership always carried on with firms name, but for the joint venture, no such firms name is required.

The persons who run the business on partnership are called as partners and the persons who agreed to take the project as joint venture are called as co-venturers.

Normally, a partnership is constituted for a long period (including various projects), whereas joint venture is formed to complete a specific job/project.

Partnership is governed under the Partnership Act, 1932, whereas there is no enactment of such kind for the joint ventures. However, as a matter of fact in law, a joint venture is treated as a partnership.

There is no limit specified for the numbers of co-venturers, but the number of partners is limited to 10 under banking business and 20 for any other trade or business.

Liability of a partner is unlimited and may extent of his business and personal estate, whereas under joint venture, liabilities of co-venturers are limited to the particular assignment or project agreed upon.

Joint Venture and Consignment

Major differences between joint venture and consignment may be summarized as −

Relationship − The co-venturers of a Joint venture are the owners of a Joint venture, whereas relationship of a consignor and consignee is of owner and Agent.

Sharing of Profits − There is no distribution of profit between a consignor and consignee, consignee only gets commission on sale made by him. On the other hand, the co-venturers of a joint venture share profits as per the agreed profit sharing ratio.

Ownership of Goods − Ownership of the goods remains with the consignor. Consignor transfers only possession to the consignee, but every co-venturer of a joint venture is the co-owner of the goods/project.

Contribution of Funds − Investment is done by the consignor only. On the other hand, funds are contributed by all co-ventures in a certain agreed proportion.