Article Categories

- All Categories

-

Data Structure

Data Structure

-

Networking

Networking

-

RDBMS

RDBMS

-

Operating System

Operating System

-

Java

Java

-

MS Excel

MS Excel

-

iOS

iOS

-

HTML

HTML

-

CSS

CSS

-

Android

Android

-

Python

Python

-

C Programming

C Programming

-

C++

C++

-

C#

C#

-

MongoDB

MongoDB

-

MySQL

MySQL

-

Javascript

Javascript

-

PHP

PHP

-

Economics & Finance

Economics & Finance

Selected Reading

Define cash books and its types

The word “cash” represents the monetary instruments (currency etc.) and the word “book” represents the record available in written format. Thus, a cash book can be defined as the record of business transactions in a particular period.

In other words, a cash book records all transactions of cash receipts and disbursements (includes both bank deposits and withdrawals). Cash book is divided into two parts namely, cash payments and cash receipts.

Transactions which are not recorded or are excluded in cash book are as follows −

- Transactions related to bank (payments made through checks in receiving or paid).

- Non-cash transactions.

- Discount making or discount received.

Cash book satisfies objectives of journal and a ledger

Cash book as journal

- Just like a journal, it records transactions in chronological order (as it happens).

- Follows the same procedure in posting transactions to ledger from cash book.

- Maintains special cash books for cash transactions.

- Records cash transactions according to debit and credit.

Cash book as ledger

- Same format as ledger.

- Follows the same T format as ledger.

- Cash book balances are transferred to trial balance.

- Serve purpose of cash account.

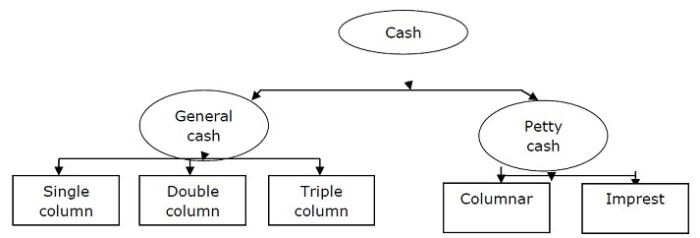

Types

The types of cash book are as follows −

Updated on: 2022-05-13T07:29:06+05:30

668 Views

Advertisements